Bessent’s Bank Warning…

Expect a wave of mergers in the regional and community banking space in the year's second half. Here's who to follow on that trend.

Good morning:

In March 2023, the collapse of Silicon Valley Bank sent shockwaves through the U.S. financial system. There was no warning.

As I’ve said, you can’t find a single article before March 7, 2023, on the crisis. That day, our Momentum Signal went negative, and we weren’t sure why. A few days later… Silicon Valley Bank was gone.

As we enter mid-2025, Treasury Secretary Scott Bessent has implied that regional and community banks are not out of the woods.

Bessent warned that without reform, some could face an extinction event.

Let’s dissect what Scott Bessent is saying.

Another Consequence of Central Banking

Bessent, former Soros CIO and one of the few voices openly challenging the Fed’s current regime, argues that U.S. Treasury yields are no longer just pricing in inflation or Federal Reserve policy.

For the first time since World War II, they’re shadow-pricing sovereign credit risk.

This means that markets are beginning to consider the possibility that the U.S. government itself may not be financially invincible.

That changes the system's structure, especially for banks that have long depended on government securities as “safe” capital.

Regional and community banks are loaded with long-duration (the bonds don’t mature for a longer time) assets, such as mortgage-backed securities, Treasuries, and commercial real estate (CRE) loans.

As interest rates surged in 2022–2024, the value of these holdings plummeted.

By Q4 2024, U.S. banks had $483 billion in unrealized losses, a 32% jump from the previous quarter. 34 banks reported paper losses exceeding half their core equity capital. You’ll recall that the Fed had to create a lending program that accepted these bonds at par value and provided collateral in return.

Commercial real estate will start to appear in the headlines very soon again, too…

You’ll recall all the warnings about CRE a few years ago. It’s not a problem for everyone - just the targeted banks with significant exposure in the post-COVID world.

Roughly $570 billion in commercial property loans mature in 2025—much of it held by regional lenders. Office vacancies remain historically high, and refinancing at current rates is often uneconomical. With real estate values down and interest costs up, defaults are rising. Regional banks, which underwrote these loans in a zero-rate world, are now exposed to a storm they can’t hedge away.

Then there’s the narrative about funding.

Deposit flight hasn’t slowed—money continues to flow into money market funds and short-term Treasuries. The issue is that even stable banks are prone to social media-style panic when these stories hit the headlines.

The run on Silicon Valley Bank was the first Twitter-induced mass panic bank run. Even if it didn’t make logical sense to some of the best minds in the business, we can’t expect every American (well, even 80% of Americans) to understand how fractional banking works.

In theory, these pressures require smaller banks to raise deposit rates to stay competitive, squeezing net interest margins and impacting profitability.

Meanwhile, regulators aren’t easing up. The proposed Basel III “Endgame” rules will raise capital requirements (how much money they have to hold) even further, hitting the same banks already on the brink.

What comes next is predictable: consolidation. And that’s where the opportunity exists.

We’ll start to see deals pick up in the second half of this year, especially with Bessent bringing this up. While trade dominates the conversation today, if we look out a few months, this appears to be a significant priority for the Treasury Department.

Opportunity is clear in the regional and community space.

Valuations are depressed. Banks are trading for well under their book value. Stronger banks are eyeing smaller players, not only for growth, but also for survival-by-scale.

Private equity firms and mid-tier national banks are poised to act as acquirers.

What we could see is not creative destruction, but defensive consolidation.

Bessent focuses on re-pricing everything in the financial system—from Treasuries to trust itself.

And for regional and community banks, deal flow is likely a survival instinct.

The good news is that there’s a lot of opportunity ahead on the M&A side.

The same factors that were driving deal flow were already present: technology costs, cybersecurity, aging board members, the need for deposits, and more.

But now you’re adding a structural issue that will drive more M&A in the second half.

In a few weeks, I’ll sit down with my father-in-law, Tim Melvin, to discuss the opportunities ahead. But it’d be smart to take advantage of the situation and familiarize yourself with this space and why the banks are a great alternative asset.

You can check out his Free letter on Substack, right here. He’ll explain the metrics you need to use… and help you find the best banks to buy.

In Focus

This morning’s bounce comes from Trump’s first official trade deal since the tariff mess began.

The UK agreement lifted markets, sending S&P futures back toward the 5,700 ceiling and pushing momentum to +38.

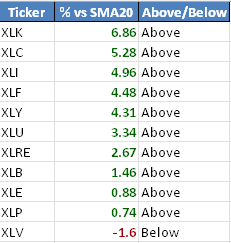

Selling pressure has vanished—for now. Every sector is back above its 20-day moving average except healthcare, with tech leading the charge.

Adding to the strength, word leaked late yesterday that the White House plans to roll back Biden-era chip export restrictions. NVIDIA started ripping around 3:35 p.m. and hasn’t slowed—it’s now up 5%.

The broader market has room to grind higher as long as that continues. But if NVIDIA fades, the rally loses steam with it. For now, the bias leans bullish as traders look ahead to trade headlines with China this weekend.

So is this the breakout or the start of another bull trap?

That depends on follow-through. The UK deal is a start, but the market wants more, especially signs of progress with China, India, or Mexico, before it starts pricing in a real unwind of trade risk. Until then, we’re still stuck in a range.

Today’s a good day to hunt short squeeze setups. Focus on beaten-down names at highshortinterest.com with clean charts and room to run—not junk. SolarEdge (SEDG) and PureCycle (PCT) are two we’re watching. If the market holds up, both could quickly move toward their 200-day.

Keep an eye on the VIX, too. Futures dropped 3.5% overnight and gapped lower. If VIX climbs back toward 23 or breaks outside today’s range, that’s your signal to reassess.

We’re on squeeze watch—but stay tactical. Not much has changed yet.

S&P sector SMA20s to start the morning:

Market View

Market outlook:

Bond yields climb after Powell signals no rush to cut rates amid trade uncertainty: 10-year up 3bps to 4.30%

Oil up 1.9% with WTI at $59.20 following bullish EIA report showing larger-than-expected inventory decline

Gold rebounds to $3,350 after Powell warns tariffs could cause persistent inflation

Chip stocks climb as Trump reportedly prepares to cancel Biden's AI export controls; Nvidia up 3.1%

Bessent-Lutnick sovereign wealth fund proposal submitted; timeline extended as administration debates implementation details

Google shares sink 6% after Apple executive says AI search will replace traditional search engines; AAPL shares fall initially before full recovery

Momentum - Momentum Holds, Watching Small Caps

Momentum held at +20 on Wednesday, with the market closing green across the board despite a midday fade. We logged 24 breakouts against four breakdowns—MRNA, BLDR, MHK, and TRGP. Seven sectors ended the day green, while staples, energy, healthcare, and industrials continued to lag.

The Russell 2000 briefly flipped yellow intraday and is now clinging to its 50-day moving average. If small caps lose that support and start to roll, they could pull the broader market down, especially tech, which remains heavily crowded.

Futures got a boost from Trump’s surprise “major trade deal” announcement, with reports pointing to the UK. That gives the market a short-term lift, but it doesn’t change the bigger picture: positioning is still light, and just a few names drive momentum. Watch small caps. If breadth on the Russell gets worse, this can flip fast. Stay on your toes.

READING

GREEN (weakening)

Insider Buying: A Little C-Suite Action (Blackout Period)

The ratio of Buys to Sells: 1:52 ($7M to $397M)

Top Buy: 2.6M of NKGen Biotech (NKGN) by CEO Paul Song

Top Sell: $137M of Roblox (RBLX) by President & CEO David Baszucki

Liquidity

While markets focused on Powell’s pause, the more urgent liquidity story came from Treasury Secretary Scott Bessent. In testimony this week, he told Congress the U.S. is “nearly out of time,” warning that the debt ceiling is pressing and the cash situation is tight. He laid out $2.5 billion in new IRS cuts and said deeper reductions are coming as the administration scrambles to conserve capital.

That pressure isn’t front and center in markets yet—but it will be. The Fed held rates steady and acknowledged growing risks regarding inflation and unemployment. The 10-year yield dipped to 4.26%, and traders still expect three cuts this year, but Powell offered little clarity.

Globally, liquidity has climbed to $177 trillion, per Michael Howell.

So while central banks aren’t easing directly, capital is moving. For now, that flow is covering a lot of cracks, but Washington’s margin for error is getting thin.

Stay positive.

Garrett Baldwin

I like Bessent more and more each day.

Off subject question: How can the SWAP market be larger than FX? Things are happening at warp speed, but it seems as though we have no compass.