Good morning… a reminder: if you can’t watch the video, we put all the content we will cover in this email every morning.

If you can join us live, I’ll be here in 10 minutes.

Hello… I’ll be live soon… and I’ll be covering the PCE report right away…

Then, we’ll dive into the insight below…

Turns out…

Not a lot has changed overnight.

The market is in a holding pattern ahead of tomorrow’s PCE report, and the most important thing we can do today is not get in our own way.

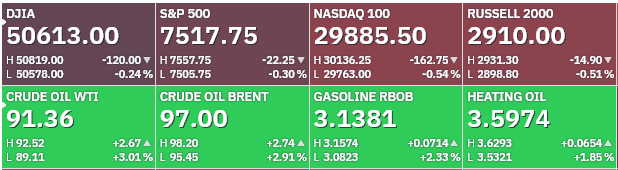

Oil remains the main driver and has been for weeks. WTI is back above $90 this morning, Brent at $97, both ticking up after some additional overnight skirmishing.

The Iran talks continue, and the deal framework is still being negotiated. While that plays out, this market continues to push higher on the back of the AI narrative, which will go on until somebody starts to question the capex spend and what it is buying.

Everybody gets excited about the spend and chases it downstream, and everything inflates. That is the cycle we are in.

The bigger story is the collision between two forces.

On one side, you have the buy-the-dip, all-roads-lead-to-inflation crowd pushing equities higher. On the other hand, the bond market says someone has to pay for this, and if the Fed does not take inflation seriously, yields will do it for them.

We’ve seen this play out. A hot print comes in, whether it is jobs, CPI, PPI, or PCE. The bottom 80% of the index sells off. The big caps pull back but maintain enough momentum to keep the market from crashing. You get a few days of repricing and some chatter about hikes. Then the buy-the-dip crowd steps back in, and the process starts over.

If this is the rhythm for the summer, then every major report becomes the catalyst. Going into those moments, we ease off the gas and make sure we are prepared for either direction.

If you are trading energy right now, OILU bounced off its 100-day moving average yesterday and is pushing higher this morning. We have seen oil bounce off these levels multiple times, and yesterday was the spot to take a shot long with a tight stop. Trust the setup.

The VIX continues to trend lower, now under 17.

The FNGD is pulling back, which gives us conviction that this market can stay irrational longer than people realize.

The FNGD is representative of margin buying among some of the market’s largest names.

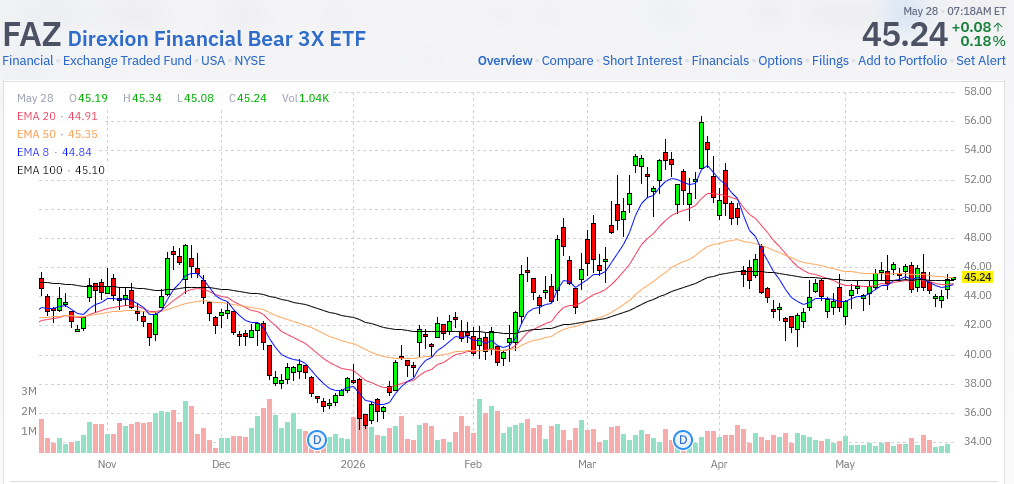

The one chart showing concern is the FAZ, which has popped back up into its range over the last couple of days. Not a cause for alarm yet, but it is moving in the wrong direction.

It does not align with what we are seeing in bond volatility, where the MOVE index has been trending back toward 70, taking pressure off the yield curve.

The 10-year has dropped nearly 20 basis points in just over 10 days since Vanguard called the short-term top. We are steadying around 4.5%. We would like to see it move lower. If it turns back up from here, the hike conversation heats back up.

Looking across our screamers this morning, the first fourteen names are all tech. After that, you get a sprinkling of everything else. Humana (HUM) is hitting the list. Centene (CNC) is back and remains our only confirmed cheap momentum name from the triples list. It looks like it could be building a base to make another move.

Oracle (ORCL), Jabil (JBL), Agilent (A), Caterpillar (CAT), Dollar Tree (DLTR), Hormel (HRL), and Keurig Dr Pepper (KDP) are also joining. Consumer goods and industrials are starting to participate alongside health care. The base is broadening.

Not much to report from the crasher side. Devon (DVN) is the only energy name on the list, which pulled under its 100-day this week and has been fighting its way back. If oil pulls back further, expect more energy names to show up there.

Salesforce (CRM) reported last night. The stock took a hit after hours but is recovering this morning after beating estimates and raising full-year guidance.

Dell (DELL) reports after the close today and is already up about 4% premarket on a new DoD deal. If Dell interests you, let it cool down first. Look for a pullback under the 8-day and target a put spread back around $240 if you can get it. Wait until after earnings.

Today, we get our next inflation reading with PCE.

There’s no reason to expect relief in this number yet. Oil may be pulling back now, but $90 crude is still high, and the elevated prices of the last few months are baked into this data.

If you’re not the type to sit glued to a screen all day trading around the reaction, consider putting on a cheap hedge heading into the number.

Something like buying TZA shares and setting a tight stop. If the market overreacts to a hot print, you have some protection.

If nothing happens, you cut it and move on. After what we have seen the last few weeks, it makes sense to have something in place.

Market outlook

Treasury yields hold ground with 10-year at 4.49% as Iran flare-up tempers Wednesday’s rally

Oil rebounds with Brent at $97 as fresh US strikes in Iran revive Hormuz disruption fears; WTI tops $91

Gold drops to a two-month low near $4,400 as rising real yields cap haven demand; silver opens down 2%

Minneapolis Fed’s Kashkari says inflation fight tops Fed priorities with prices too high; energy and fertilizer costs flagged as key drivers

Dell (DELL) lands $9.7B Pentagon software deal to provide Microsoft (MSFT) 365 and cloud subscriptions; deal follows Dell’s $6.25B Trump accounts pledge

Benioff defends Salesforce (CRM) amid AI disruption worries; accelerates buybacks to $27.1B, stock slips 1.5% after-hours on soft guidance

Copper traders rush to ship metal to US as renewed tariff speculation reignites global squeeze; Comex positioning most bullish since 2020

Momentum - Cruising

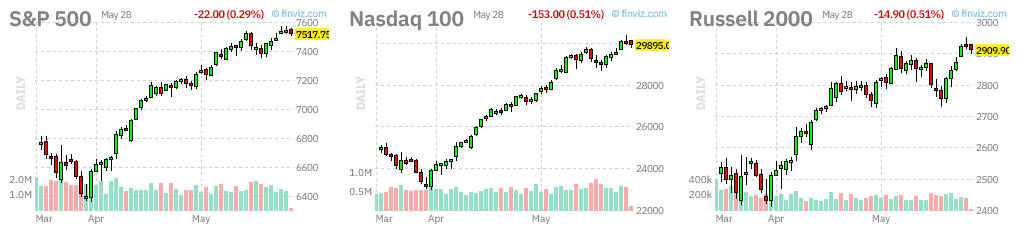

The market drifted on Wednesday with the S&P and Nasdaq basically flat on the day. The daily momentum readings have been bouncing around this week, but the trend underneath hasn’t changed. The anchors are holding steady. S&P at +52, Nasdaq at +19 and +23, Russell at +38 and +66. All three indexes are still firmly positive on the weekly and monthly readings and the crasher counts remain low across the board.

Consumer cyclical names led on Wednesday at nearly 1.5%, which is notable because a week ago, discretionary was under pressure and sitting beneath key moving averages. Now it’s breaking out again. The WANT ETF, the triple-bull consumer discretionary fund, is up over 5.5% in the past week. That kind of turnaround in a sector that was lagging tells you the capital behind this rotation is real, not just a one-day bounce. Tech pulled back slightly on the session and energy continued to take the brunt of the oil repricing, down nearly 2% on the day and 6.5% on the week.

On the broader weekly view, consumer cyclical is up over 5%, basic materials and tech are both near 5%, and industrials are up 4.6%. The buying keeps finding new places to go, which is what you want to see in a market sustaining a move. The daily readings bounce around. Russell’s equal-weight pulse dipped slightly negative this morning while the cap side held, a minor divergence worth watching. The trend underneath is what matters, and right now it’s clean.

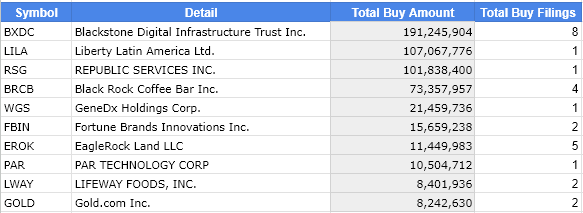

Insider Buying: Huge Buy Carries The Day

The ratio of Buys to Sells: 1:7 ($122M to $832M)

Top Buy: $107M of Liberty Latin America (LILA) by Director John Malone

Top Sell: $187M of Twilio (TWSO) by Director Andrew Stafman

Top Insider Buys of Last 10 Days - Form 4 Documents

Market Liquidity

The funding side of the system is comfortable right now. SOFR has dropped about 7 basis points below the fed funds rate, which in plain terms means banks have enough cash on hand that borrowing overnight against Treasuries is cheaper than borrowing without collateral. That’s what ample reserves look like in practice. The MOVE is back to 70, and the bond market digested a full week of auctions without breaking a sweat.

Underneath all of that, the credit picture keeps getting worse. Private credit defaults set another record in April. Consumer delinquencies are back at levels that haven’t been normal since 2008.

Companies that borrowed heavily when rates were low are running out of ways to manage the payments now that rates aren’t. A lot of them are finding creative ways to push the problem forward rather than deal with it, which works until it doesn’t.

And this is where it gets tricky. The system can have plenty of cash and still be building toward a problem if the borrowers drawing on that cash are slowly going underwater. Rates are the bridge between those two realities. As long as yields remain elevated, the funding markets can function well even as the credit quality of the people using them continues to deteriorate.

That disconnect is sustainable right up until it isn’t, and you rarely get much warning when it flips.

June has a lot packed into it.

The first FOMC under new leadership happens on the 16th.

It also features, triple witching, the biggest quarterly expiration of the year, on the 20th. Inflation data that will shape how aggressive the rate conversation gets heading into summer.

The plumbing feels good right now.

What it’s carrying is another story.

Stay positive.

Garrett Baldwin