Thank you B.S.Smokey, Damian, william mcleod, LiquidityProblem, Veronica, and many others for tuning into my live video!

Here is the PDF from today’s conversation…

10:10 reading… for June 5

Me and the Money Printer

5

LIVE - What Investors Are Getting Wrong... And What Lies Ahead

Everyone, everywhere now an expert on Japanese cross-border flows...

Jun 05, 2026

Good morning…

I’ll be live at 8:30 am right here..

Good morning:

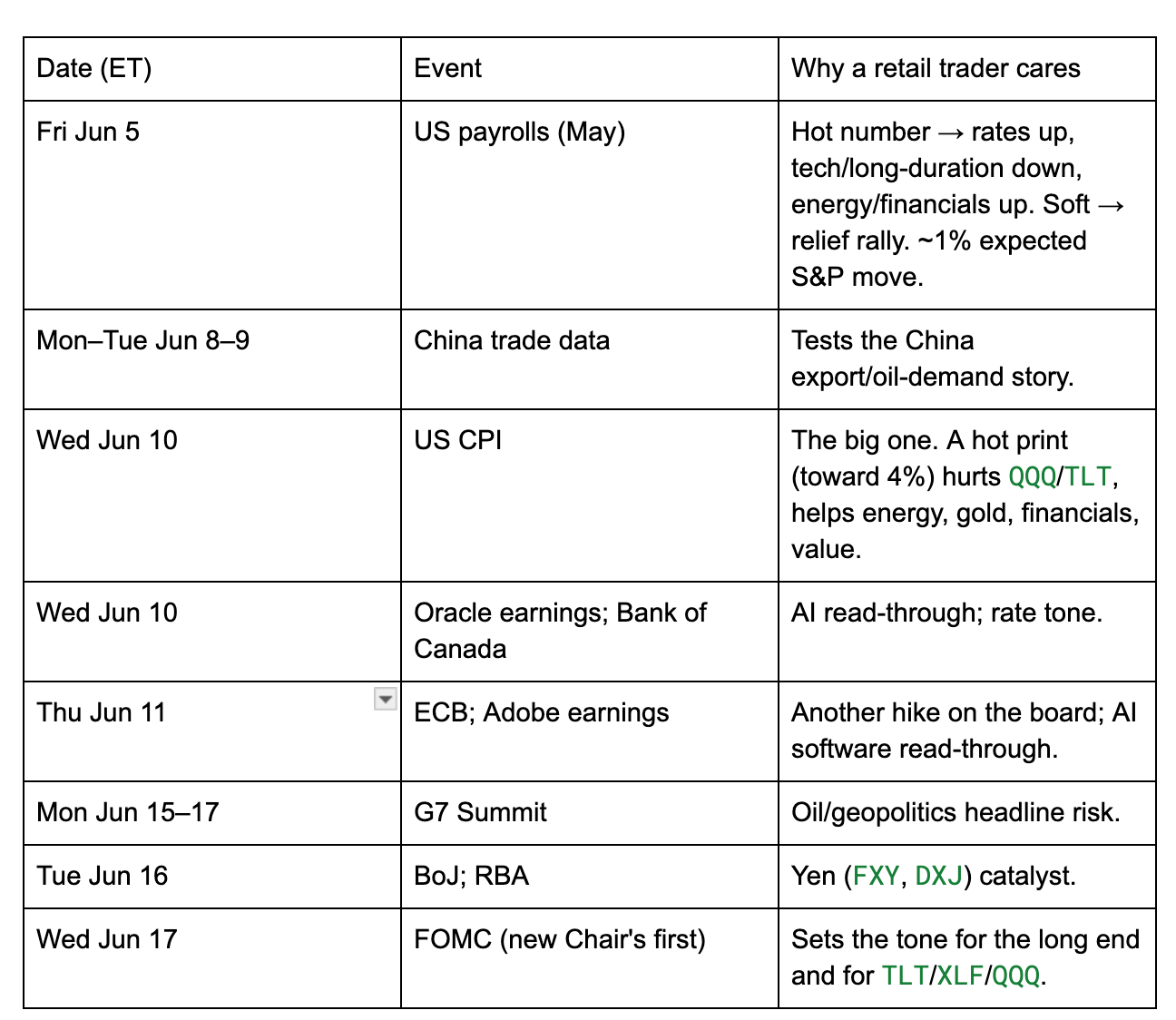

I start today with a loaded schedule over the next week. We have a string of potential landmines that must be navigated.

It’s all heavily focused on data that will tell us just how healthy the plumbing in the global system is. And it culminates with Third Friday (OpEx) on June 19.

So… let’s go Thunderdome…

On Japan

The most important story in the next two weeks is Japan’s interest rate decision.

I must go back to a May 17 article in the Financial Times for context.

The surge in Japanese yields are triggering big bets that domestic investors will repatriate their money. Japanese investors own something like $6 trillion in foreign assets. And I’ve said that flows BACK to Japan could trigger broader selling in leveraged positions here in the U.S. and maybe even lead to passive selling too…

Okay, the story is no longer the property of macro tourists on social media.

It was in the FT with named institutional voices on the record.

Again, this is the number one macro risk I have flagged all year.

The day Japanese money decides it has been overseas long enough. It would especially hit U.S. Treasuries hard, given that Japan is the largest single foreign holder. This ownership has been a leverage layer beneath every dollar-denominated bull market of the last generation.

The Bank of Japan meets Tuesday. The market is pricing a hike to 1%. That would be the highest level in a generation (1995).

But… let me walk you through what’s happening now…

Japan Is the World’s Banker

For 30 years, the Bank of Japan ran interest rates at or near zero.

Japanese savers and institutions had to look elsewhere for yield.

They found it in the United States through Treasuries, stocks, real estate, and yes, private credit. According to the FT and BoJ Flow of Funds data, Japanese investors are by far the largest foreign holders of US government debt.

Most of the pile sits unhedged.

And, therefore, an unhedged Japanese investor in American assets is long the U.S. dollar by default.

Each time that the dollar got stronger or the yen got weaker, that investor was paid in two directions.

Assets went up in price, and the currency went up in translation. For three decades, the carry trade was more or less… “free.”

This big pile of international capital has helped support U.S. asset prices for 30 years.

I can’t say that this was the intent… but it was the math.

The third-largest economy in the world parked half of its institutional balance sheet elsewhere. The markets received that capital trade at much higher mulitples than they should have. The American equity multiple is partially a Japanese subsidy.

Three Pillars Can Crack at Once

This is where it gets dangerous.

There entire reason why an unhedged Japanese investor would want to stay in American assets rests on three legs of the same stool…

They’re all weakening right now.

First, yields in Japan are rising. They’re the highest in decades.

Their five-year and twenty-year bonds both both recently hit record highs that same week. For an institution that held foreign bonds because domestic bonds yielded nothing, the domestic alternative finally yields something.

Next, the BoJ WILL hike its interest rate to 1% on Tuesday.

Again, that’s the highest Japanese policy rate since 1995. The expectation is that we’ll see 1.25% sometime in 2027…

And every time they hike, the more attractive domestic rates are to Japanese investors...

Finally, the yen at 160 is historically cheap.

An unhedged investor returning home converts dollars at a favorable rate by any long-run measure.

Now, Japan’s Finance Minister Satsuki Katayama has admitted this set up is there…

She told reporters that government bond yields are rising across the world’s biggest bond markets and that, in her words, these developments are creating a compounding effect.

So… now… if you accept this framework, the question of when Japanese money rotates home is not whether, only when.

Institutional Money Is Already Positioning

Matt Smith, a fund manager at Ruffer, told the FT in May that pressure is building, that long-end domestic yields are rising, and that the institutional framework in Japan is now please bring this money home.

Smith said yen strength will happen slowly, then quickly.

How would this happen?

The unhedged Japanese investor holds a U.S. Treasury or a U.S. equity.

To bring the capital home, the investor sells the asset in dollars, receives dollars, then sells the dollars to buy yen. The selling shows up as three simultaneous moves. U.S. Treasury yields rise. U.S. equity prices fall. The yen surges against the dollar.

If a small share of the $6 trillion pile moves at once, the moves are absorbable.

If a meaningful share moves in the same direction in a compressed window, the moves are the August 2024 carry trade unwind on a larger scale.

The Nikkei fell more than 12% in a single session that morning.

The S&P fell more than 6% across three sessions.

The leverage that unwound was the cross-currency carry trade built quietly over decades.

The Loaded Gun Is Not Yet Fired

But I want to stress something… this is all a big headline story…

And right now, Wall Street just isn’t seeing the flows just yet.

Japanese investors haven’t taken the bait of rising JGB yields.

The reason, per Keshvani, is that Prime Minister Sanae Takaichi has been clear about her preference for more fiscal spending. The supply of new JGBs will not fall meaningfully.

If yields keep going higher because supply keeps going higher, investors are reluctant to step in front of the move.

Japan’s financial plumbing data tells the same story.

The Ministry of Finance’s International Transactions in Securities release shows the Banks line has turned negative since the start of the year, which is the first signal of Japan Post Bank selling.

The BoJ Flow of Funds report through Q4 2025 shows Post Bank bought more JGBs and also continued buying foreign assets.

The signal has not yet flipped.

Now, let me highlight the most important part of this…

GPIF, the Government Pension Investment Fund, is the investor that really moves the yen.

GPIF holds nearly $1 trillion in foreign assets, invests mostly unhedged, and sets the template private pensions follow.

GPIF completed its five-year strategy review in 2025.

The next is not due until 2030.

Its targets are locked. GPIF can rebalance within its policy bands, with roughly $85 billion of capacity to rotate, but the published quarterly data shows GPIF and private pensions have continued buying foreign debt and selling foreign equities through the latest reporting period.

Effectively, trying to guess when this is going to happen is an impossible task. So, we have to continue to watch the plumbing and the GPIF. And we have to actually focus on our signals as they tell us where to look. Remember, our S&P 500 signal turned negative on August 1, 2024. Four days later was the implosiion of the Nikkei.

So, I want to stress that it’s likely to happen gradually then suddenly…

We’ll continue to keep our focus on the flows through our Momentum Signal.

What To Watch

If the BoJ signals reduced JGB purchases at the same time it hikes, the yen rallies hard and the carry breaks faster. The hawkish surprise is the bigger move than the hike itself.

Any move that narrows the gap is a step closer to GPIF making the math work. A Fed cut, a soft US payroll print, a sudden disinflation surprise, any of those narrow the gap and move the institutional rotation closer.

The 160 line is the Ministry of Finance intervention level. A break below 160 toward the 150s is the first signal that real money is rotating, and that the unhedged repatriation has begun.

Remember, this dog has not barked.

But the dog is still in the room.

There is about $6 trillion leaning against a door marked home.

It will be there… but don’t bet until we actually see evidence or real justification for flows. This is the single most important macro story that I’m watching like a hawk…

Now, let’s get to the trader update…

Good Morning,

Traders Focus

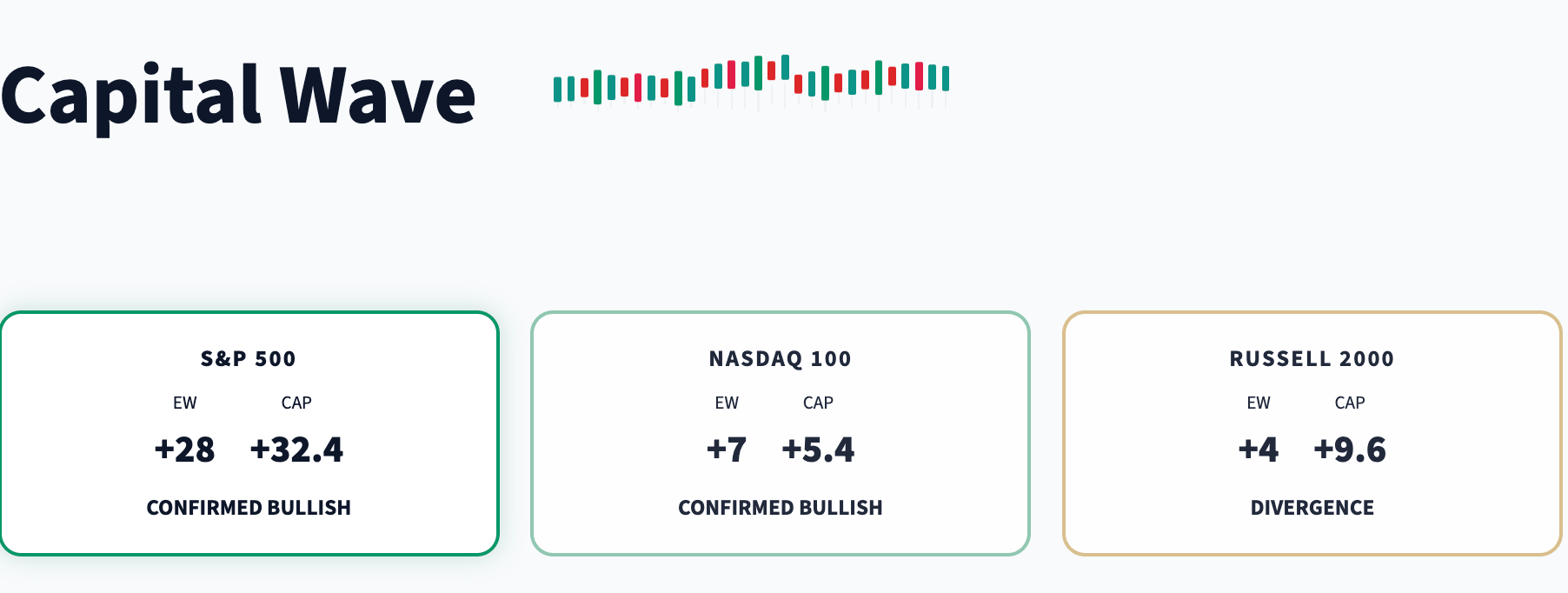

As we await this morning’s jobs report, momentum continues to pull back in the short-term readings across all three indexes.

This has been the story all week. The names that ran the hardest got stretched, and now the air is slowly coming out of them.

You can see it in the bigger readings too. A week ago, the S&P cap-weighted side sat at +151, with the equal-weighted side at +62. Five days later, the cap is down to +52, while the equal-weight holds at +46. The money is leaving the biggest names, the ones that have been carrying things higher.

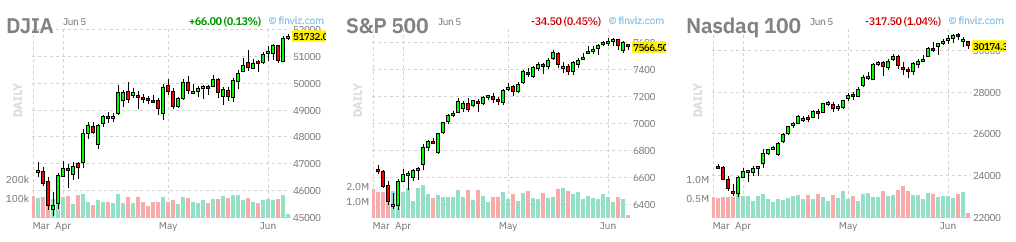

This is part of the concern. If capital is leaking out of what has been working, the market stumbles unless it rotates into something else. Yesterday it rotated, and the Dow closed at a record while the Nasdaq went red.

This is a lot like a car racing down the highway. The driver is easing off the gas now. We are still moving, just a little slower, and now would be a good time to brace in case he has to hit the brakes. He could just as easily floor it again, so be ready for both.

The job numbers today will be a big decider. Consensus is around 85,000, down from the 150,000 average over the last two months, with unemployment holding at 4.3%. Anything above that keeps the Fed handcuffed.

Watch the wage number, not the headline. A hot wage print is what drags the rate-hike conversation back to the front. But a number that comes in too soft has its own problem, because it feeds the story that AI is starting to eat jobs. Tech alone announced more than 38,000 cuts in May, the heaviest month in two years, with AI the top reason cited.

Options are pricing about a 1% move on the S&P off the number.

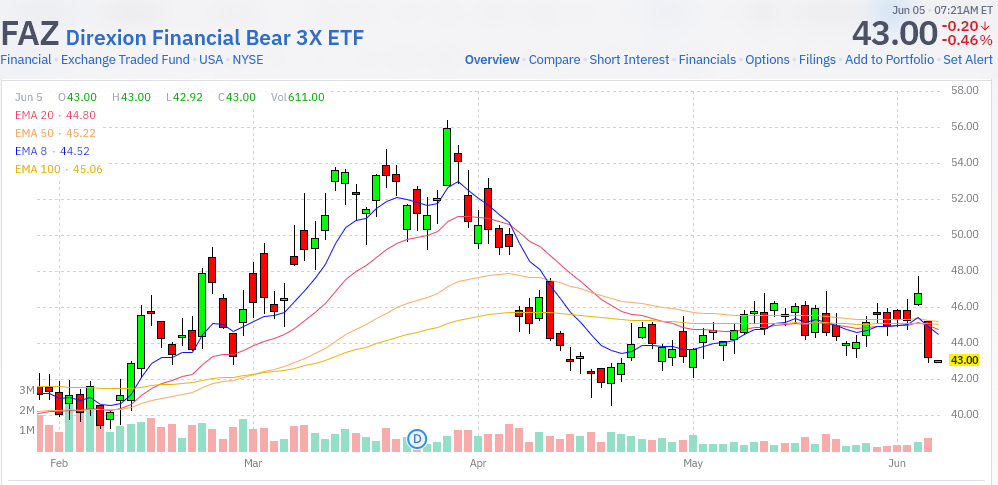

The one bright spot this morning is the FAZ, the 3x bearish financials ETF we watch as a read on the financial sector. It fell almost 8% yesterday, a big improvement, even if it feels strange against what crypto is doing right now.

The FNGD is our bigger concern, jumping almost 5% yesterday and still climbing toward its 20-day moving average. This is where we start pounding the desk about keeping one eye on your Six Rules of Negative Momentum and one eye on the door. The semis are sitting right at their 8-day, and the MAGS (the Magnificent Seven ETF) is fighting to hold its 20-day. The warnings are building. Not screaming yet, but growing.

Take the sugar away from a market that has been running on a sugar high and you get some cranky behavior. Crypto and the Russell are the first places it shows up.

Crypto pulled back again overnight, with Bitcoin down to around $60,000 and Ethereum really taking it on the chin at a new low near $1,668, a level we have not seen since last year.

Coinbase (COIN) is getting hit hard. If this is all about the SpaceX IPO next week pulling air out of crypto, it is a little funny, because Coinbase just launched pre-IPO perpetual futures on SpaceX. These guys are doing it to themselves.

Oil eased slightly overnight, with WTI at $92.50 and Brent at $94.50 after Trump softened his tone toward Iran. The OILU is back above its key moving averages, so the sector remains elevated. The dollar remains pegged around 99, where it has sat for the last month.

We are still seeing some real rotation right now, which tells you money wants to stay in the market and just change seats.

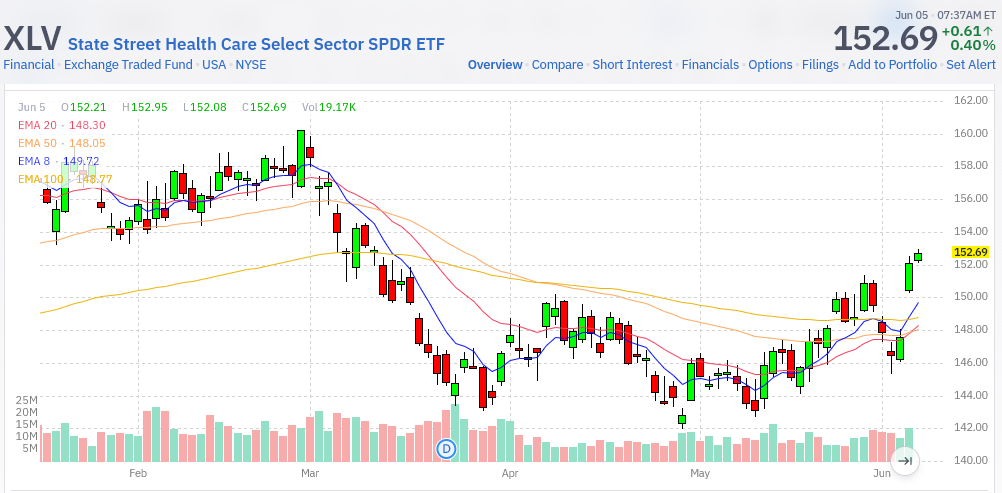

Health care is breaking out. Eli Lilly (LLY) and AbbVie (ABBV) are hitting our breakout list. If you want to play the group, the XLV is a cleaner way to do it than the LABU, which holds some of the higher-beta names. The cap-weighted names are doing the lifting in health care right now, so the XLV is the better ETF there.

DaVita (DVA), GM, NXP (NXPI), and Norwegian (NCLH) are also new to our screamers this morning.

Albemarle (ALB) is one to watch on the crasher side. It finally cracked under its 100-day after a monster run, up more than 300% since last year’s Liberation Day low.

That puts a name we like in sale territory. It has held the $157 level more than ten times, so that is where you look for your best entry. Lithium sits at the center of the battery, data center, and EV buildout, and the government is leaning in. We want the trades the government is backing.

Utilities are under some pressure, with Constellation Energy (CEG) on day two of our breakdowns. If you like the space, this is the time to take a small taste on names like Constellation, or lower your cost basis if you already hold. Dominion (D) has held up better than Constellation lately.

A couple of earnings to watch today around VWAP, with options expiring. Planet Labs (PL) beat and raised its 2027 outlook but is down about 3.5% premarket. Into the SpaceX hype next week, this is a name to trade off VWAP. Look for a pullback and a shot higher.

Lululemon (LULU) is getting crushed on its report. If it fights back toward $110, that is where you take the short into the close. If it pushes back above, you are wrong, so just cut it. It is a one-directional trade.

We are going to wait for the jobs reaction, let the first fifteen minutes shake out, and then use VWAP to target the names expiring today for the bigger swings.

On a pivot day like this, the play is not to guess direction. It is to have your levels charted in advance.

Know your entries, your targets, your stops, and where you sit relative to VWAP before you put anything on. The moment a trade does something outside your plan, cut it, because the reason you got in is no longer valid. This is a market where you have to be disciplined, or you end up a bag holder.

For now, the music is still playing. We keep dancing around the chairs, making sure we are close to a seat when it stops.

Market outlook

Treasury yields drift lower across the curve before jobs print; May payrolls seen slowing from April’s 115,000 with rate at 4.3%

Gold consolidates near six-week lows as Iran war drags on; metals weighed by central banks countering energy-driven inflation shock

Trump invokes Defense Production Act for coal; $700M investment includes new export terminal in California and new plants in Alaska and West Virginia

Lululemon (LULU) cuts full-year outlook as incoming CEO O’Neill inherits sluggish growth; stock down 11% afterhours

Sempra (SRE) starts LNG production at ECA Phase 1 in Mexico with first cargo from Permian Basin; Pacific Coast location offers shorter Asia route than Gulf

S&P keeps megacap IPO rules unchanged for S&P 500 after consultation; SpaceX (SPCX) and other mega-IPOs must still serve 12-month seasoning

Momentum - Holding

The AI names pulled back Thursday and the rest of the market picked up the slack. Broadcom fell about 13% on a soft outlook, taking the chips down with it, leaving the Nasdaq as the only index in the red. The S&P still closed higher, the Russell ran more than 1.5%, and eight of eleven sectors finished green. The money rotated out of the AI trade rather than leaving the market.

The trend readings backed it up where it counts. The Russell’s equal-weight anchor, which had slipped below zero on Wednesday, is back to +19, and the anchors are positive across all three indexes. The daily side stayed whippy, surging into Thursday’s close and cooling again overnight, but the trend readings that drive the signal held the ground the rotation gained. The one soft spot is the cap-weight, where the chips carry the most weight and where the selling landed.

Healthcare led the day at better than 3%, with financials and real estate behind it, and tech was the only group down by any real amount. The move into the value names ran strong enough to push the Dow to a record even with the AI trade selling off. The leadership changed hands for the day, with the broad market carrying the load the AI names usually do.

Insider Buying: Still Underwhelming

The ratio of Buys to Sells: 1:72 ($14M to $1B)

Top Buy: $4M of Xometry (XMTR) by Director Alexander Biewald

Top Sell: $221M of NVIDIA (NVDA) by Director Mark Stevens

Top Insider Buys of Last 10 Days - Form 4 Documents

Market Liquidity

The thing that’s quietly changed under this market is the flow of money into it. For most of the year it was getting topped up. The Fed was still buying bills, and with US rates sitting so far above everyone else’s, foreign money kept pouring in. That’s fading now, and a few things are pulling it the other way at once.

Central banks are tightening again. Europe is expected to raise rates next week, and Japan is likely to follow at its meeting the week after. As their rates come up, the gap that made US assets the place to park money narrows, and some of that foreign cash starts to head home. The Fed’s next move is now seen as more likely to be a hike than a cut. And the wave of giant IPOs led by SpaceX is about to pull a lot of cash out of the market all at once.

You can see it starting to show up in the data. The Chicago Fed’s financial conditions index spent the spring loosening, then flattened out, and has now begun to tighten. It isn’t dramatic, but the direction is what matters. For the first time in this run, conditions are getting tighter rather than easier, and they’re doing it with stocks still at record highs.

That’s the setup heading into summer. The market’s holding up fine on the surface, still near its highs. But the easy part is probably behind it, the stretch where money kept showing up on its own looking for a place to go. From here it has to hold these levels with less and less help underneath.

Stay positive.

Garrett Baldwin