We Know, Jamie

The bank that has benefited more than any other from the Fed's policies for 112 years now warns about the bond market.

Dear Fellow Traveler:

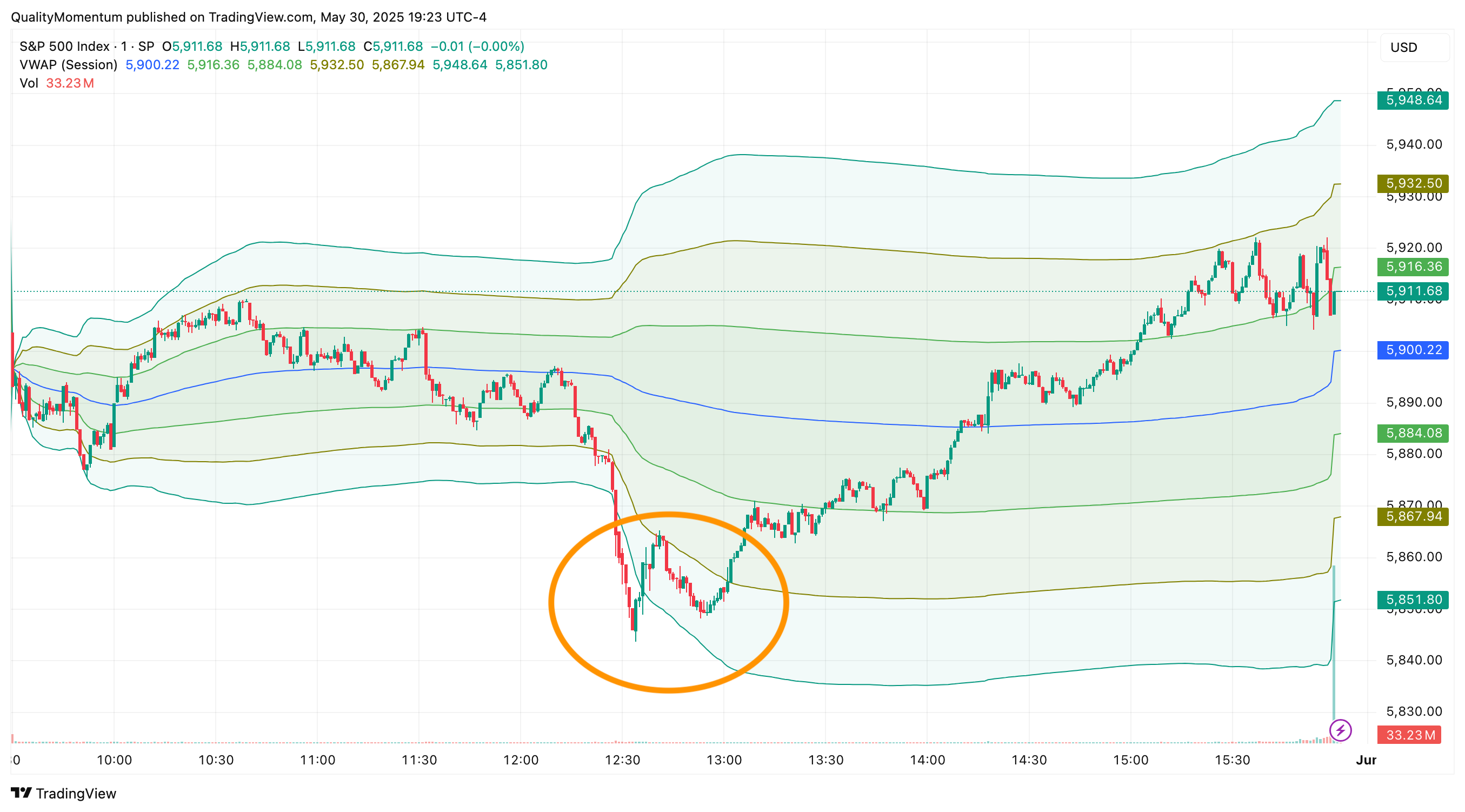

This afternoon, I was trading Volume-Weighted Average Price (VWAP) when something curious happened. The S&P 500 fell into the fourth standard deviation of the one-minute VWAP.

See that orange Circle… that’s an overreaction…

You’re seeing that - in a short period - S&P 500 dropped way more than normal, far outside its usual range.

The fourth standard deviation is extremely rare. Most price moves stay within 1 or 2. Hitting the fourth means the market was acting unusually volatile or extreme.

So… what happened?

Jamie Dimon is worried about the bond market. He was speaking today… right then.

At today's Reagan National Economic Forum, Dimon warned that excessive spending by the U.S. government and the Fed’s massive quantitative easing programs would lead to a "crack" in the bond market.

Not if. When.

He says it could be six months or six years. But it's coming. And when it does, he told regulators point-blank: "You are going to panic."

There’s so much to unpack here…

I Love Jamie Dimon’s Teffon Nature

If we put this warning another way…

It goes…

The JPMorgan Chase CEO, who's been dining at the Fed's all-you-can-eat liquidity buffet since 2008, warned that the cheap money party will eventually end.

For anyone keeping score…

JPMorgan is the bank that took over Bear Stearns with Fed backing in 2008.

It bought out Washington Mutual during the crisis.

It also scooped up First Republic's carcass in 2023 for pennies on the dollar.

Those were cheap gifts over the years.

Most people don’t know that the bank ran an “Ambassador Program” out of Washington, D.C., ahead of the Dodd-Frank Act in 2009-10.

This massive PR and lobbying blitz put employees in the rooms with politicians, where they shared talking points about how the bank wasn’t trading leveraged derivatives ahead of the 2008 Financial Crisis… and were one of the good guys.

As a result, JPM helped shape Dodd-Frank, which imposed massive compliance burdens that crushed smaller banks, while JPMorgan’s scale let it absorb the costs and dominate.

Dodd-Frank was the regulatory mistake that told everyone that the government would rescue mega banks in a crisis.

This lowered JPM’s funding costs and attracted deposits.

As derivatives moved to central clearing, JPMorgan became a dominant clearing member, earning billions in fees and gaining visibility into client trades.

That happens when you help shape the regulation.

And JPM used its influence to shape other rules in its favor, expanded into client trading and payments, and captured business competitors.

This company has thrived in the last 17 years of perpetual economic crisis.

Remember the Bank Term Funding Program (BTFP) that saved regional banks in 2023? JPMorgan had access to that risk-free arbitrage candy store, too.

It has surfed every single wave of Fed intervention.

Every time the Fed floods the system, JPMorgan gets first dibs on the cheap capital.

It then turned around and made a fortune lending it out… or who knows, doing what else. This is a place that doesn’t just benefit from the money printer.

They practically co-authored the instruction manual.

But Here's the Thing...

Now, Dimon isn't wrong.

I've been writing about the return of the "bond vigilantes." Here, I’m talking about those investors who dump treasuries when they smell fiscal irresponsibility.

I've been tracking the cracks forming in "the financial system's plumbing."

Foreign demand for U.S. treasuries?

Slipping.

We’ve had five black swan events in the last six years, and we've already experienced multiple four-sigma events in the bond market in the previous four years.

For those keeping score at home, a four-sigma event is supposed to happen every 63 years. In 2020, Treasury markets froze, and the Fed had to go full throttle to restore basic function, and so much money that cotton prices tripled (but not solely because the dollar is made from cotton and other composites).

Then, in October 2022, we saw the UK pension fund implode due to leveraged bond positions. In March 2023, Silicon Valley Bank discovered that "risk-free" treasuries can still blow up a balance sheet.

In August 2024, the Nikkei crashed over worries about the carry trade.

And that April crash we had? It only reversed because of fears about the bond market… cracking.

We don’t have black swans anymore.

We have a regular flock circling our heads.

The Real Warning

So what is Dimon warning?

He's warning that the next crack might be THE crack.

And that’s fair - I thought the COVID crash was THE crack.

THAT crack is where there's no bid when the Treasury tries to auction debt.

It’s the one where a major institution faces forced liquidation with no buyers.

It’s the one where the Fed's tools finally stop working.

Each crisis since 2020, we've managed to steady the situation.

Dimon's saying the next wobble may be where the entire damn breaks.

Of course, I don’t think Dimon’s warning us out of the goodness of his heart.

Having witnessed JPMorgan’s marketing and public relations reach in Washington, D.C. during graduate school, I consider this strategic positioning at its finest.

First, it's about covering Dimon’s assets.

When the bond market does crack, Dimon can say "I told you so…" And everyone will say that he was some oracle… not the guy who benefited from the very policies that would ultimately fuel that final crack.

Second, notice how he's pointing fingers at regulators and government spending?

Not at the banks that lobbied for every loophole. Classic blame shifting.

Third, guess who'll be there with a Fed backstop to buy distressed assets at fire-sale prices if panic does hit?

It's the same playbook from 2008 and 2020 with better PR.

And he’s playing the game.

The bond market IS fragile. Foreign buyers ARE stepping back.

The Fed IS running out of magic tricks.

And when the music stops, there might not be enough chairs.

The fact that the warning comes from someone who helped create the problem doesn't make it less true. It’s just important to see who benefits in the end.

As I've been reminding readers, when it comes to the money printer, there's no such thing as "free."

Someone always pays.

And it's usually not the banks.

Stay positive,

Garrett Baldwin

Thanks Garrett. Great stuff.

Can you comment on the possibility that the frequency of black swan events is related to algo (increasingly influenced by AI) trading? In 1987 (grad school...yes I am old), someone I can't remember the name of came to Stanford to give a seminar IN THE ENGINEERING DEPARTMENT on short term forecasting of the stock market (eigen-modes and such) and how to exploit 8 minutes of future performance to make a pile of money. The discussion period was fixated on the notion of this question: What fraction of the trading following such a strategy would lead to feedback (stabilizing or destabilizing) that could then "drive" the market?

I don't know about you but wherever I click these days I get about 50% ads to hook retail investors into AI guided training. You can say I must have clicked one of them to get that frequency but in fact I have skipped them all. Given that frequency, I have to figure they ARE getting "takers" for this (ads cost money) and this makes me wonder how much of the story about retail investors supporting the bubble (told as a confidence measure when all the studies say otherwise) while smart money has pulled back is driven by AI guided "algo" trading? Of course AI is "learning" its own feedback but, if its objective function is to capture short term gains without a significant penalty (like ALL investors have) for sharp downturns this seems like it has to end badly.

So, I will ask some curious questions (that are 38 years old...probably older than half of the retail market):

1) what fraction of retail trading do you think is currently AI guided? (is there any data on it)

2) what fraction do you think is the "tipping" point- where investing on principles and reasoning becomes meaningless because all that matters is what AI thinks of the signals?

Put another way, you mention watching for these 3 and 4 sigma events that are expected every 63 years but already they are a couple times a year and, if my concern is valid, we should expect them to be more and more frequent to the point that, if nothing is done to de-incentivize this (some sort of trade friction...seems what we have is insufficient), we are at the mercy of watching the markets either self destruct (crash or other) or just become a game of trying to catch black swans (at which point that name is meaningless if not already).

Well, with that happiness, I'll have to add my two favorite baseball players, the problem is they're both tied for first!

I'm from Houston so I'll say Nolan Ryan first and then mention my other #1 is (drum roll please) Cal Ripken Jr. Bless them both for longevity! Can you believe 2,632 straight games, all with Baltimore?