What If We’re All Wrong About De-Dollarization?

Reconsidering the "Death of the Dollar" story...

Dear Fellow Traveler,

The biggest macro consensus of the last three years has centered on one trend…

De-dollarization.

That’s the ongoing shift away from the U.S. dollar by other nations. There is no shortage of ongoing calls about the “Dollar’s Death” - arguments that dominate financial media, newsletters, and observers.

I’ve written about this subject extensively… and certainly posited that this has been a one-way trend that had started to snowball…

But today… I’ll challenge my own assumptions… and that broader narrative.

The story goes that countries are moving away from the dollar as a reserve currency, buying gold, and looking for an escape hatch to price commodities in other currencies.

We hear about the BRICS and other resource-rich nations turning away from America.

Gold prices have more than doubled since the Ukraine war began.

And we recall that the U.S. Treasury played a massive role in creating dollar skepticism… It froze Russia’s central bank reserves after the invasion… roughly $300 billion in assets, locked up overnight. The message to every other central bank on earth was clear. Their dollar reserves were only theirs so long as the U.S. approved.

We didn’t just sanction Russia... We stress-tested the entire concept of “reserve assets”… and then acted surprised when everyone started looking for the exits.

Central banks responded rationally to the Treasury’s actions.

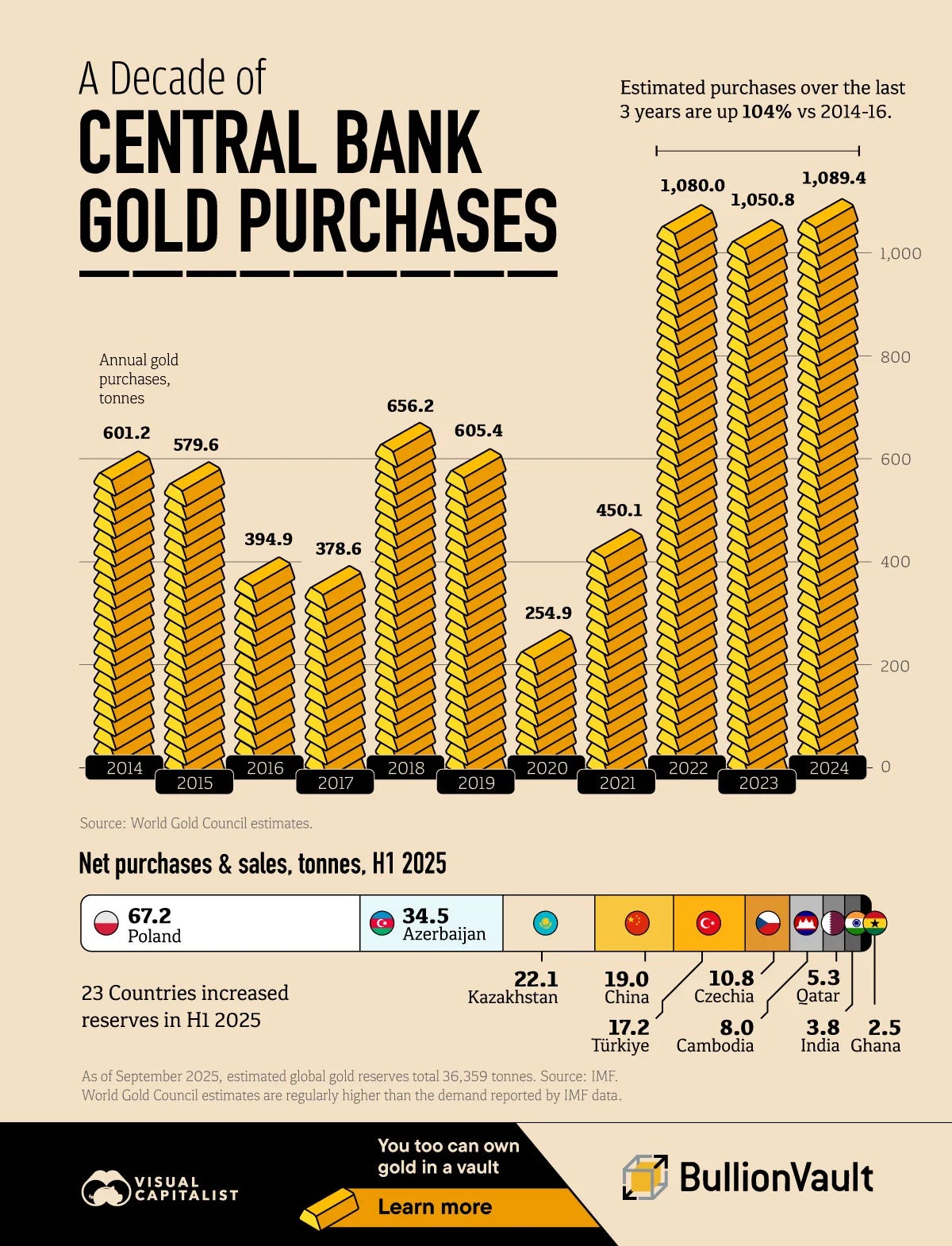

China, India, Turkey, Poland, and more started buying gold at record levels.

Between 2022 and 2024, we saw the largest central bank gold purchases in decades, and the pace remains elevated relative to historical norms.

Dollar reserve holdings as a share of global reserves have been declining for years… though the dollar remains dominant compared to other fiat currencies.

As the BRICS nations started building alternative payment systems, the narrative became a consensus… a groupthink direction that de-dollarization is here, the dollar’s dominance is fading, and gold or Bitcoin is the primary exit.

Now, I ask… what if we’re wrong about that pace… or even the one-way flow…

Last year, I wrote a piece called “Have All of Us Gotten Bitcoin Wrong?” in which I explained that Bitcoin isn’t what people think it is… The story people tell about Bitcoin and the outcomes that it produces, I found, are two different things.

Today, I want to explore whether the same misread is happening with de-dollarization.

A recent academic paper in the International Journal of Political Economy suggests it might be.

The Paper

All week, I’ve dug into the GENIUS Act, the Clarity Act, and the plumbing of the stablecoin infrastructure.

A reader, intrigued by the commentary, sent me a copy of an academic study from February 2026.

So, I dug into it yesterday…

From that paper, I have deduced that maybe… just maybe… the United States has pulled a rabbit out of its hat… and found a way to circumvent foreign central bank activity and even bought more time for the greenback than the dollar skeptics expect.

The paper is “Monetary Sovereignty in the Digital Age” by Jack Buchan and Murat Üngör at the University of Otago in New Zealand.

The paper questions how countries should maintain control over their own monetary systems in an era of digital currencies.

Such an answer could shift the entire de-dollarization debate…

As the authors explain, the biggest threat to global monetary sovereignty isn’t Bitcoin, a Chinese digital yuan, or a rogue blockchain protocol run by a guy in a hoodie.

“The primary digital threat” is private, regulated, dollar-denominated stablecoins…

And the GENIUS Act is what legitimized and scaled them...

According to global CBDC trackers, more than 130 countries representing the vast share of global GDP have explored or are now exploring central bank digital currencies as a defensive response to crypto assets, foreign CBDCs, and what the paper calls “the immediate and more potent channel”… regulated dollar stablecoins.

Central bankers didn’t wake up excited about innovation.

They woke up realizing their currencies might be getting quietly replaced by an app.

Digital Re-Dollarization

The paper calls the stablecoin movement (the kind I’ve discussed all week) “digital dollarization,” and the mechanism is simple.

Someone in an emerging market downloads an app on a phone.

This app lets them hold USDC or USDT instead of their local currency (created by their local central bank…).

As an example, think of someone in Europe holding digital dollars on their phone instead of Euros, which are managed by the European Central Bank.

These people hold USDC or USDT because the dollar is more stable (and it is…), the app is easier, and the stablecoin settles instantly on rails that don’t close for holidays or because the nation is suddenly wartorn.

Remember, no government ordered them to do something, and no treaty was signed.

They… at the individual consumer level… decided to switch to dollar-backed assets…

When enough people switch, the central bank’s monetary policy tools can start breaking. The authors write on Page 5…

Digital dollarization may occur through two primary channels: (1) when cryptocurrencies or, more consequentially, globally accessible stablecoins gain widespread adoption within a state’s domestic economy, or (2) when a foreign CBDC is widely adopted, effectively replacing the local currency for everyday transactions, savings, and reserves. This phenomenon undermines the state’s ability to exercise control over its monetary policy and financial oversight.

That last sentence is the outcome of the two primary channels… and it’s damning.

Central banks can’t manage inflation through interest rates if a meaningful portion of their economy has opted out of their currency entirely.

They can’t conduct monetary policy on money they didn’t issue.

The paper’s language is worth quoting for its insights into how stablecoins impact their autonomy.

On page 17, the authors say stablecoins are…

These stablecoins pose a more insidious and potentially pervasive challenge than any foreign state-issued CBDC. They penetrate domestic markets through existing digital platforms and apps, offering technological efficiency while channeling economic activity through foreign-denominated instruments beyond national monetary control.

The paper doesn’t fully offer a conclusion on the second-order effect that I highlighted above... But I’ll point this out.

When stablecoins are backed primarily by short-term Treasuries and cash equivalents, global adoption doesn’t just shift currency usage.

It tends to create incremental, structural demand for U.S. government debt.

That demand doesn’t require a central bank decision, treaty, or permission.

Funny enough, it also doesn’t even require awareness.

Again… it happens at the user level… one wallet at a time.

The Counterstrike

At the institutional… central bank level, the de-dollarization story is real.

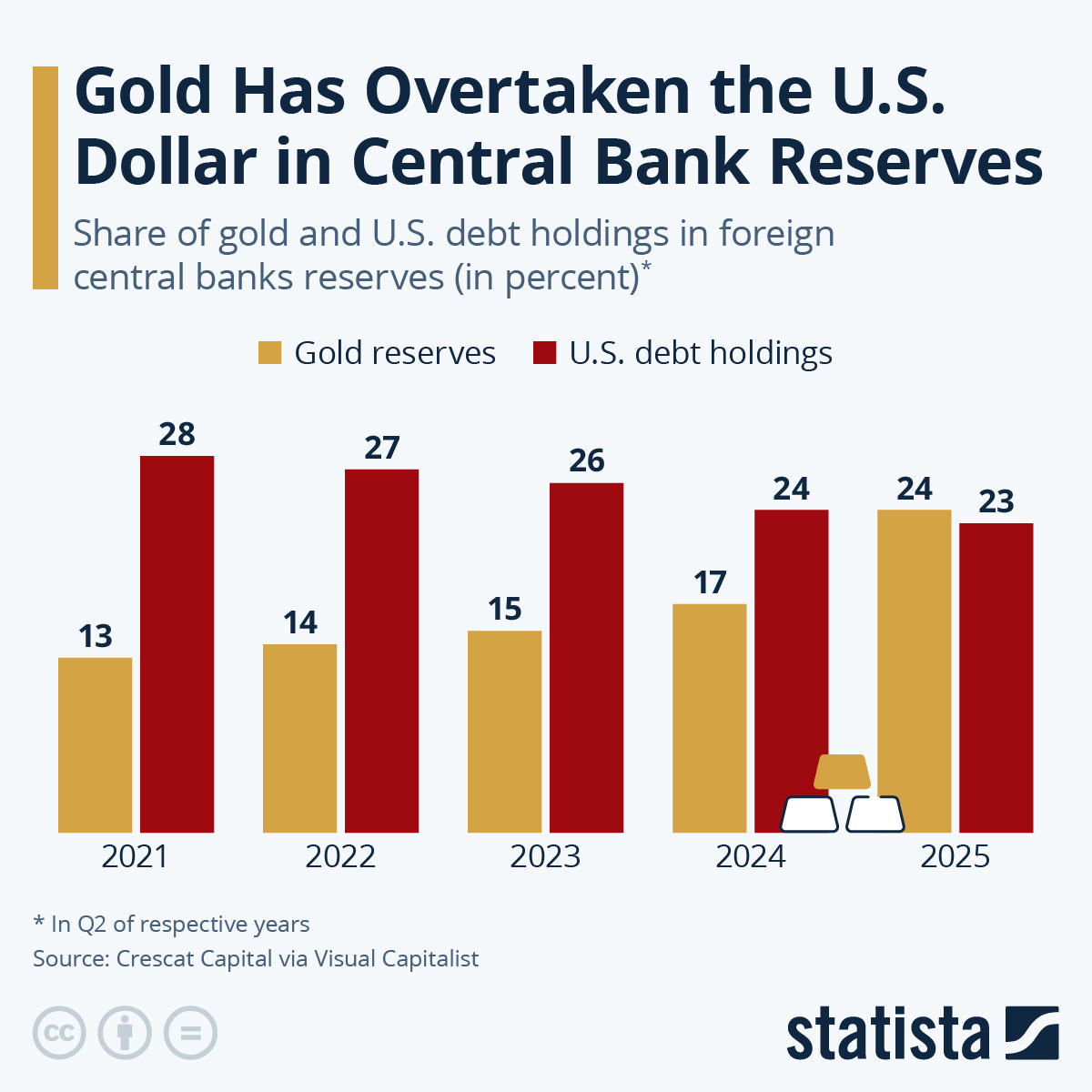

Central banks are diversifying away from Treasuries. That is what drives the “Death of the Dollar” narrative. We can see it in the charts… like this one from Statista.

But the assumption underneath the narrative… that this means the dollar is losing its grip… is challenged by the stablecoin expansion.

Everyone is watching central banks sell Treasuries and buy gold.

But we need to start watching what happens one layer below.

The GENIUS Act is significant…

Congress didn’t build a digital dollar.

It franchised one… and gave it a balance sheet.

In practice, the Treasury doesn’t need central banks to hold dollars.

It doesn’t live or die on whether sovereign wealth funds buy Treasuries.

Instead, stablecoin activity starts with the citizen… the person in Istanbul, Lagos, or Jakarta who downloads an app and holds USDC because their local currency lost 30% last year and the stablecoin didn’t.

I’ll remind you of two things about foreign demand and why it matters…

First, when I went to Argentina 12 years ago, I learned quickly about the difference between the official exchange rate and the Blue dollar exchange rate. The average Argentinian couldn’t access dollars and wanted them because of their eroding currency. People everywhere made me offers (well above the official exchange rate) for any dollars I had in my pocket…

Second, this has already been stress tested during the Liberation Day panic in April 2025. The dollar index didn’t explode higher as it had in previous crises in 2008 or 2020. Instead, researchers found that in nations where targeted U.S. tariffs were higher, demand for stablecoin surged. Whether it was a coincidence or a straight-up test case of what would happen, the Federal Reserve of Cleveland found that foreign investors loaded up on these assets in expectation of tariff enforcement.

It wasn’t central banks buying dollars… it was foreign citizens.

And that’s the point.

Now imagine they can access all the dollar-backed stablecoins with instant settlement, 24/7, however they want.

Such a scale at the micro-level would develop a never-seen-at-scale dynamic where the institutional layer is de-dollarizing… while the consumer layer is re-dollarizing from underneath, one wallet at a time, through private rails that don’t pass through any central bank.

And that matters - because speed, settlement, and privacy matter in a world where individuals move a lot quicker than bureaucracies.

Central banks hold meetings, but people hold phones.

One of those scales a hell of a lot faster.

The Difference Is Clear

In practice, regulated stablecoins are backed primarily by short-term Treasuries and cash equivalents.

So every person who opts into a dollar stablecoin is creating a tiny, automatic, non-discretionary bid for U.S. government debt that their own central bank just sold.

Foreign governments are debating the dollar.

Their people are quietly buying it.

The central banks are selling Treasuries at the top of the capital stack.

The citizens are buying them back at the bottom… through stablecoin reserves… without even knowing that’s what they’re doing… and in some ways they don’t care because they want whatever can preserve purchasing power.

Gold doesn’t do all of this.

It sits in a vault and doesn’t create fiscal demand or fund government deficits.

A dollar stablecoin on a phone in Brazil does both… it gives the holder a stable currency, and it effectively forces a T-bill purchase into existence.

So, I ask about the pathway here…

What if de-dollarization at the sovereign level is happening at exactly the same time as re-dollarization at the individual level… and the individual level scales faster?

The mechanism is real, but the magnitude is an open question.

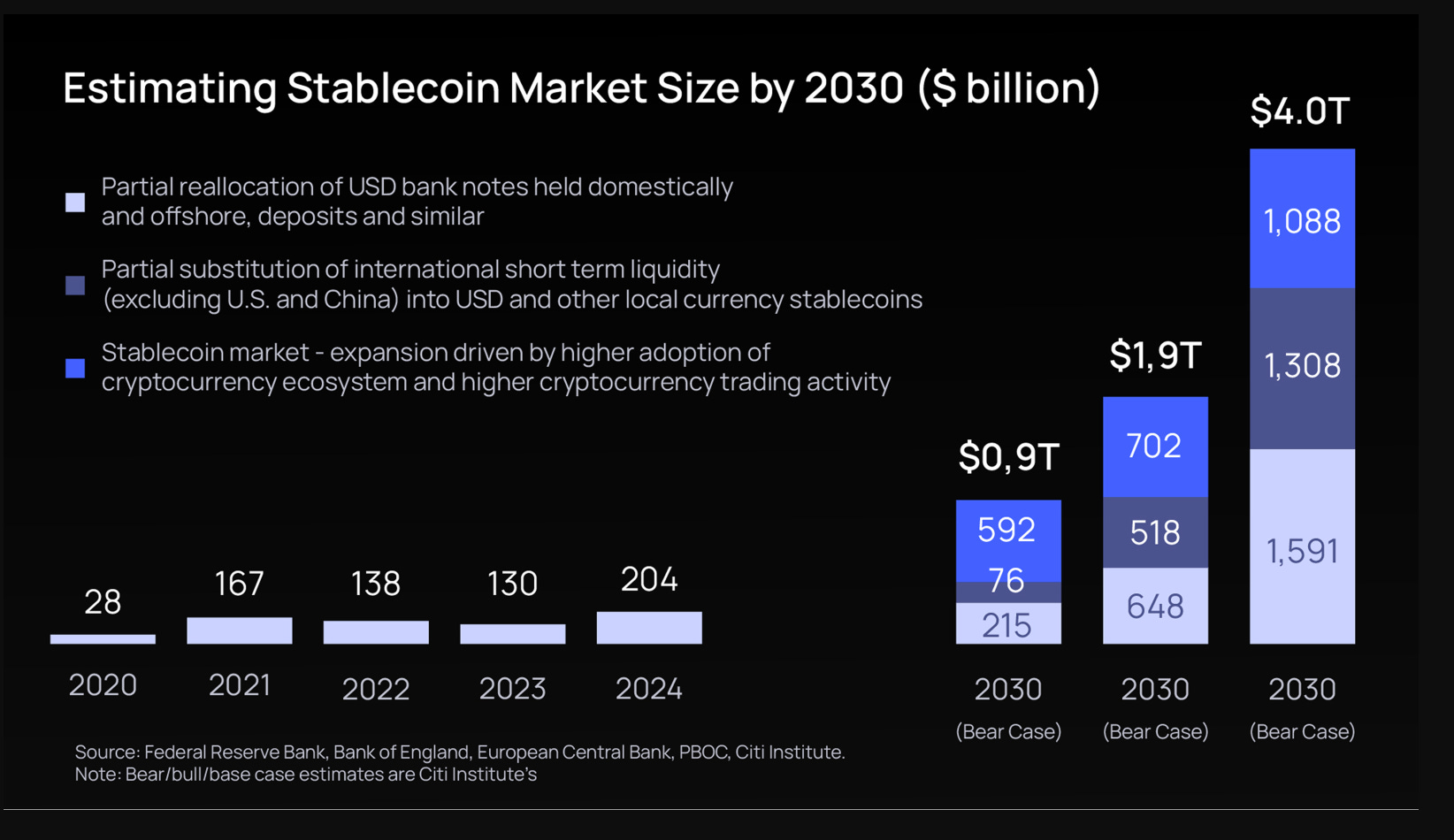

The stablecoin market cap is in the hundreds of billions today, not trillions.

Some projections suggest the market could scale toward the trillions.

TreasurUp.com suggests that the stablecoin market has significant expansion potential… (Note: it appears they errored on their chart, and the $1.9 trillion is the base case, while $4.0 trillion is the bull case.)

We’re not there yet. But the direction and the goal are clear.

And What About The Paradox

The Buchan and Üngör paper, in its footnotes and conclusions on foreign market penetration, describes a “reverse domino effect.”

And I think this is equally important to the story above…

It seems that the U.S. deked (a hockey term for tricking an opponent) other central banks in recent years on stablecoins. And I don’t find the following to be a coincidence, but a tactic in the broader Capital Wars playing out globally.

When major economies build CBDCs, the process puts pressure on others to follow.

But the U.S., the dominant currency issuer, stepped back from pursuing a retail CBDC. It even aimed to create laws banning the Federal Reserve from creating one.

The paper’s point is subtle.

The authors note that the U.S. didn’t accelerate the race. It slowed it… and made everyone more vulnerable in the process. That U.S. policy action dampened global CBDC urgency.

Some countries thought, if the U.S. isn’t building one, then maybe we don’t need to rush either.

But the U.S. didn’t just step back from a CBDC.

It simultaneously legitimized private dollar stablecoins through the GENIUS Act.

So the countries that relaxed on their CBDC timelines are now more exposed to the very thing a CBDC was supposed to defend against.

The paper calls this a “paradoxical environment.” And that’s important… because the modern monetary system is full of paradoxes.

The authors write that countries most vulnerable to the stablecoin wave face greater urgency at the very moment the dominant player tells them there is no rush.

Game theory…

The authors also note that Nigeria launched a CBDC, but almost no one used it despite its innovation and “sophisticated design.” The government built the product, but nobody showed up, and the market created a workaround.

Other countries could try harder… through capital controls, outright bans, or CBDCs that actually compete. Whether they succeed is the open question.

What To Watch Now

The fastest-growing American export is no longer television shows about dancing or singing… but the dollar itself.

It’ll travel across private stablecoin rails, largely backed by Treasury bills and regulated under the GENIUS Act. When you layer on existing tools like Fed swap lines, which help reduce the need for forced Treasury selling during dollar shortages, the system also has a mechanism to manage the sell side.

The paper doesn’t need to connect those dots.

We already did.

Every app download is a tiny, invisible vote for the dollar as the world’s reserve currency… cast not by a central banker or a head of state, but by someone who just wants a currency that doesn’t lose 15% of its value every year.

This structure doesn’t need intent to produce outcomes.

It really just needs participants.

Right now, there are a lot of participants… and, interestingly enough, most of them don’t even know what they’re participating in.

We spent 18 years debating whether the dollar would collapse.

But have we considered the possibility that it would just… go around, everyone?

It’s worth greater discussion… and a moment away from the usual doom and gloom.

Sure, I know there are questions…

What if there’s a power outage that impacts the digital apps… what if there’s a crackdown… what if too many people think about roasting marshmallows by the fire at Camp Waconda… and a giant Marshmallow Man starts attacking the cellphone towers.

That’s all for another day…

For now… I just want to make sure that we challenge assumptions… and know the other side of the argument before making any extreme bets.

Stay positive,

Garrett Baldwin

So the Big Idea conclusion here is - buy and hold CRCL??

thought provoking article Garrett. Will this also change the thinking for gold and silver holdings? Could it possibly reduce the demand for investing in or holding gold and silver, whether physical or miner/royalty.