When the Wheels Come Off...

The next phase of leverage will be finding something to build it around...

Dear Fellow Traveler:

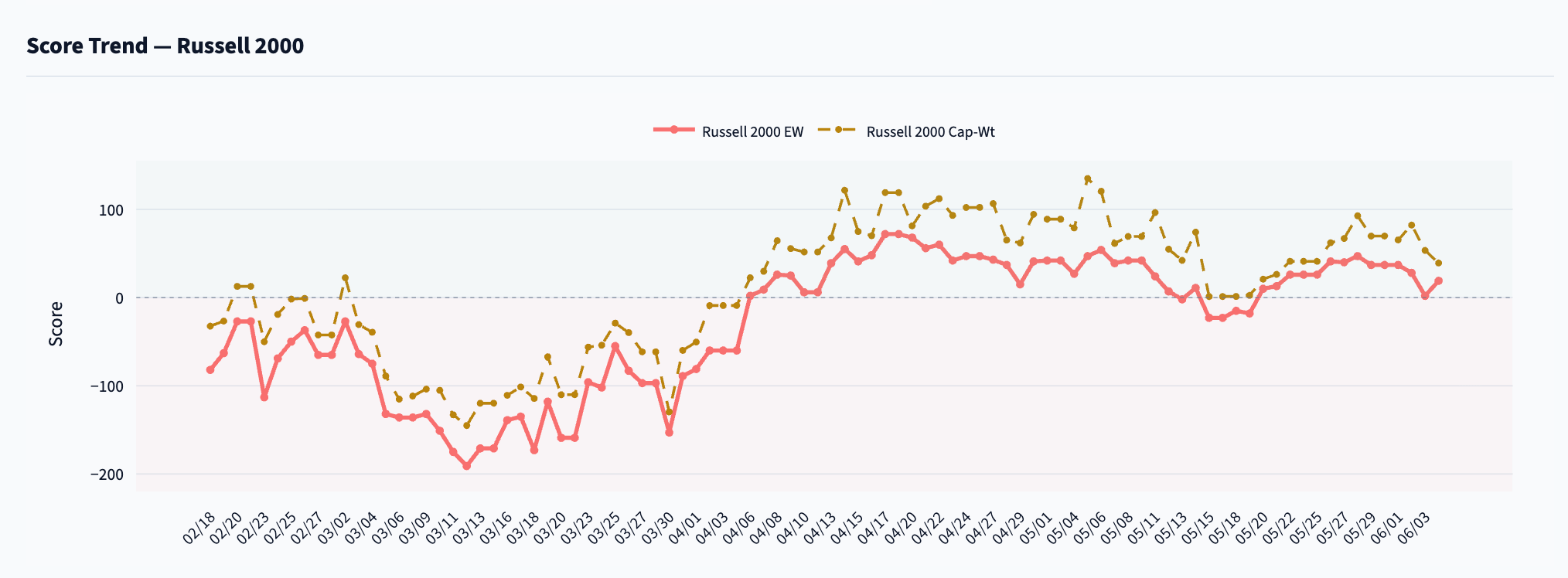

Well, the Equal Weight on the Russell 2000 turned negative in premarket hours, and it set us up for a squeeze. Markets bounce back and remain resilient… right after open.

It’s not a false signal, as the CW never went negative…

This is a reminder why I don’t tend to take direct aim at the downside of the markets unless our Cap Weight turns negative…

And even then, here we are with a bit of a pop today on… what news exactly?

This is a reminder that we’re not in a trend-driven market outside of the crowded names and the one specific trade dominating everything. Today was a short-squeeze day, and if you need proof, Chargepoint (CHPT) - that dumpster fire - popped 9.2%.

Groupon (GRPN) added 6.8% (62% short float) and 1-800-Flowers (FLWS) gained 4.2%. Another weird day, and a reminder to follow the Cap Weight and go to the downside when we break under a key moving average like the 20-day. I’m early…

But I’m hedging for a reason… Tomorrow’s jobs report comes fast…

Let’s Have Some Fun

Today, we dig into a fun topic… What’s going to happen when Wall Street runs out of ideas?

In the 2000s, it was leverage around Mortgage-backed securities.

In the 2010s, it was the growth of private credit and volatility products…

In the 2020s, it was more private credit, 0DTE options, and V-shaped, mechanical rallies…

In the 2030s, it’ll be what poor bastard is willing to sign asome random term sheet.

If I were going to bet, I’ll assume they’ll get even more creative in the off-blockchain gambling markets… hyper-leveraged decentralized crypto, and some bizarre way to 5x a Russian ping pong match on margin…

But let’s look at a few ideas that I’m happy to license to Wall Street…

Here are five things they will sell you in the wreckage (unless you join our team…)

The USA Distressed BDC Recovery ETF

Let’s launch a Distressed BDC Recovery ETF.

After all, we have some Wall Street firms opening promoting private credit investment while warning clients about the possible problems at the insurance level.

In the words of John Tuld “There’s going to be a lot of money to be made coming out of this mess and we’re going to need all the brains we can get around here.“

So, how would this work?

First, the credit cycle would just create a whole lot of wreckage that can be repackaged… hopefully for yield.

If that happens, let’s go fInd a bunch of BDCs trading at 40 cents on the dollar…

We can then go talk to someone like State Street and pitch the SPDR Distressed BDC Recovery ETF. We’ll have the ticker be BDCR.

Our pitch is that we’re buying quality balance sheets at cycle lows.

But in reality, we’ll just attach underlying assets that are the bankruptcy estate of the funds that gated sometime this year… (If the Fed prints after we lock this up… awesome, since everything can just go back to par, and we can still collect fees.)

We’ll charge an expense ratio 1.4% and try to find a way to lock up some assets for a very long time - even while we sit here using the public market like a skin suit..,

We’ll launch it the day that CNBC books a manager on Squawk Box who tells people that the “The Best Time to Buy Is When There Is Blood in the Streets.”

People will say that’s stupid…

We’re playing the game…

Let’s Launch a “Pension Allocation Rescue Vehicle”

You know that certain teachers unions are pretty ticked off that they have to buy SpaceX right now…

The fact that their passive investment flows pile into a finite number of publicly available shares at a 90x/sales valuation is a huge punch in the gut to anyone who viewed Elon Musk as a political adversary during his DOGE years…

Yeah… that’s where we are right now…

Well, let’s imagine a world where pension funds get gated out of their private credit positions and eventually need capital to fund Q4 retiree distributions.

We can ask some fund to purchase the gated positions out at like 60 cents on the dollar. The vehicle we’d pitch to a name like Apollo and call it the “Great American Liquidity Solutions Fund.”

The structure would be… really… really simple.

Check this out…

It’d just be a Cayman-domiciled feeder that lends to a Bermuda master fund that turns around and lends to a Delaware SPV that buys the LP interests directly.

It’ll take about 45 minutes to set up with Claude…

The pension fund will say thank you…

The teacher will say something else that starts with “You…”

And that portfolio manager at Apollo gets a new place to hangout in the Hamptons.

The Bank Capital Relief Trade

Don’t you for a minute think that I’ve forgotten about the poor, suffering bankers who dominate the commercial banks.

That stuff would really look bad in a stress test if central bankers did their job.

So, let’s get out in front of it…

We could propose to Goldman Sachs that they structure a credit-linked note that transfers the first 7% of losses on the bank’s NDFI book to a fund that nobody can find anywhere… not even if there is a fire...

We’d get the fund rated by a bond agency… or by the brother of a guy who works at a bond agency. As in we could say that we got the bond rated by Kroll…

But not Kroll Bond Rating Agency…

This would provide capital relief to the bank, while the fund gets a coupon payment… from the bank.

We’d allow the bank to count this structure somehow as a hedge…

Then, when someone from the Federal Reserve asks where all the risk went, we just smile and point to the dinosaur bones that we bought with all the origination fees.

Stupid?

The Delmarva Retail Whiplash Fund

Okay.

So let’s think about the retail investors.

Let’s imagine that Robinhood says - largely by accident - that retail outflows are accelerating out of private credit interval funds. That seems confusing, because I’m not sure that they really know what that is… because everytime I think of Robinhood, I think of Cricket Wireless for some reason…

Anyway, let’s say that Vanguard announces plans for a Retail Sentiment Recovery Fund, because we’ve pitched them this idea…

Basically, a fund would by whatever retail is selling at the bottom, and sell whatever retail is buying at the top.

Our fact sheet would come up with the term “Behavioral Alpha,” allowing us to basically charge something like 200 basis points and get our own personal chef.

This would be marketed on TikTok by 23-year-old influencers on TikTok who get stumped when we ask them what a credit cycle is…

It’s just stupid enough to raise $11 billion in 90 days…

Finally, Get Drunk and Gamble on Rock-Paper-Scissors

Now we get to the best idea so far…

There are two guys at a bar, but there’s only one shot of Mellow Corn for one person...

And some sort of canned light beer for the other person.

These two guys throw rock-paper-scissors. The loser shoots second in Golden Tee.

Going second means watching the first guy clear Bayou Burner clean and then trying to remember whether it was the second click or the third click that got him there.

Going second is losing.

So, JPMorgan could structure a credit default swap on the loser of rock paper scissors.

The CDS pays out when the loser loses the throw.

The credit event is documented as “Failure to Deliver Favorable Shooting Position.”

The reference entity is the specific individual at the bar, identified by driver’s license.

The contract is documented under ISDA Master Agreement with a Bar Game Annex.

JPMorgan’s quant team publishes a 147-page white paper titled: The Persistence of Throw Selection Behavior Among Midwestern Males, 2009-2028.

Their conclusion is that some guy named Brian remains fundamentally overexposed to Paper.

A competing report from Goldman argues Brian’s recent Rock usage represents a structural regime shift rather than a cyclical deviation.

The stock drops 6%.

The notional is sized at $50,000 per throw.

And the premium is paid in 12 monthly installments by Venmo.

I’ve got 15 people who will take this idea right now…

This Thing Would Snowball

By 2027, the CDS market on bar rock-paper-scissors could easily top $4 billion.

The protection buyers would be hedge funds in Greenwich.

The protection sellers could be life insurance companies in Des Moines.

Nobody in Des Moines knows who Brian is.

Brian doesn’t know who they are.

Yet somehow a retired schoolteacher in Iowa now has indirect exposure to Brian’s decision-making process after six Coors Lights and two failed marriages.

Turns out, Brian used to throw paper a lot because his ex-girlfriend liked paper…

But in 2028, a hedge fund may discover that Brian has suddenly been throwing ROCK for six straight months. By 2029, Brian’s throw history may become an asset class.

Bloomberg adds a terminal function:

BRIAN <GO>

Traders can monitor:

• Rock Frequency

• Paper Momentum

• Scissors Volatility

• Ex-Girlfriend Adjusted Win Rate

A boutique research firm upgrades Brian from Neutral to Outperform after a three-week stretch of aggressive Rock deployment.

The hedge fund buys $400 million of protection on Brian.

The hedge fund then pays the premium for 18 months.

Them, Brian thinks about his ex-girlfriend, and he throws… paper for some reason...

The CDS triggers… and the Des Moines insurer pays out.

Then, the Des Moines CIO is fired.

The CFO soon writes a letter to policyholders that uses the word unforeseen four times. There’s a classic liquidity run on top of existing problems in private credit that have gone on for the better part of there years.

The Federal Reserve wants to protect private credit, so it conveinently convenes an emergency facility to distract attention…

They call it The Rock-Paper-Scissors Liquidity and Stability Program.

The facility purchases Brian-linked securities at par. Treasury officials insist the bailout is necessary because Brian has become systemically important.

Brian remains unaware… as he just met Amber Lynn, who will be his third marriage…

He’s still at O’Malley’s arguing about whether Golden Tee peaked in 2007. He’s also still never even heard of JPMorgan… and banks at a credit union.

Finally, the Institutional Investor runs a piece titled “How JPMorgan Sold 4 Billion Dollars of Credit Protection on a Guy Named Brian.”

Someone at the bank randomly asks me if I know the editor and can kill the story…

I can’t even share my screen properly… People forget a year later…

They’ve moved on to leveraging “Pick a Number 1 to 10.”

Call It A Day…

We laugh because it sounds ridiculous.

Then again, somebody once convinced investors to buy a leveraged ETF linked to volatility futures that didn’t actually track volatility.

Compared to that, introducing leveraged rock-paper-scissors derivatives might be the most sensible product Wall Street has launched in 20 years.

This is modern finance… And the parody is less absurd than reality…

In the end… leverage wins… and leverage is the story. Don’t forget it.

Now, if you’ll excuse me… it’s Amelia’s first day of summer… and the pool calls.

Stay positive,

Garrett Baldwin

On a slightly more serious note...

Why not just market QQQMSX - QQQ minus SpaceX? I've heard ads for ETFs that represent the results of a search query on various company attributes. The overhead for packaging an ETF must be tiny. Investing in QQQMSX would be a powerful way to send a message about the quality of SpaceX's offering.

Most amusing G-man!