Inflation Is a Choice. So Is Refusing to Fight It.

Feels like we just had this conversation... 11 years ago...

Dear Fellow Traveler,

Today, The Guardian economics editor James Warner noted that the Trump Administration found itself in a situation where inflation, falling oil reserves, and the prospect of ongoing demand destruction became significant pressures.

This fueled a desire to reach a deal with Iran.

The bond market screamed multiple times during the war. It took several public statements and perhaps improvisation to pull markets back from the edge and to force bond sellers to reconsider their positions as the war continued.

The threat of persistent inflation and higher yields reminded me of the James Carville quote from his time in the Clinton Administration. He said that if re-incanation exists, he wished to return as the “bond market.”

All the while, the Federal Reserve did follow through with its efforts to maintain ample reserves in the banking sector through the first quarter (tax season), and potentially prevent another run on banks at a time that they could afford it the least.

Now, the real work begins… Inflation remains sticky - in services - an important factor given that we have remained in this state for several years. On Wednesday, Federal Reserve Chairman Kevin Warsh offers his first post-Fed meeting conference.

With the war fading from the front page, everything zooms right back into focus. Private credit, the carry trade, the basis trade, the need for more buyers of U.S. debt, and the persistent monetization of debt that has been part of our post-2008 world.

Oh yeah… and fighting inflation…

Remember Remember

Just two months ago, Warsh sat down with the Senate Banking Committee. He took questions at a witness table as part of his confirmation hearing.

Warsh’s opening statement will be quoted very often in the years ahead, especially a line where he channeled the more libertarian-leaning economists in history.

He said that inflation is a choice.

That is correct.

I just don’t think he’ll like where that sentence takes us in our discussion.

If inflation is a choice, then so is the practice of not fighting.

Starting tomorrow, he’s the one making that choice on what to do next.

Before we get going on what lies ahead, I want to point something out… so that you don’t think I’m taking crazy pills. Most people think that the Federal Reserve only has one tool to combat inflation… the ability to raise and lower interest rates.

That’s not true at all.

Like the Treasury, they have a full toolbox. Things they can do to fight inflation.

The harder question is why these tools haven’t been used more aggressively in the post-COVID era that saw record money printing and historical stimulus efforts.

Here’s the Toolbox

Yes, the biggest tool is the interest rate level.

The Fed can make money more expensive to borrow. The pipeline goes that higher rates leads to people borrowing less, which means less spending, which means prices cool…

The last time someone really used this hammer, it was Paul Volcker.

He rose rates toward the 20% level. That helped crush the inflation of the 1970s. But the U.S. government is $39 trillion in debt, and we’d now need to refinance a ton of short-term debt at much higher levels. More on that soon.

You can crush inflation with rate hikes, but there’s a cost. Volcker’s move caused a brutal recession on its way to breaking a decade of price increases.

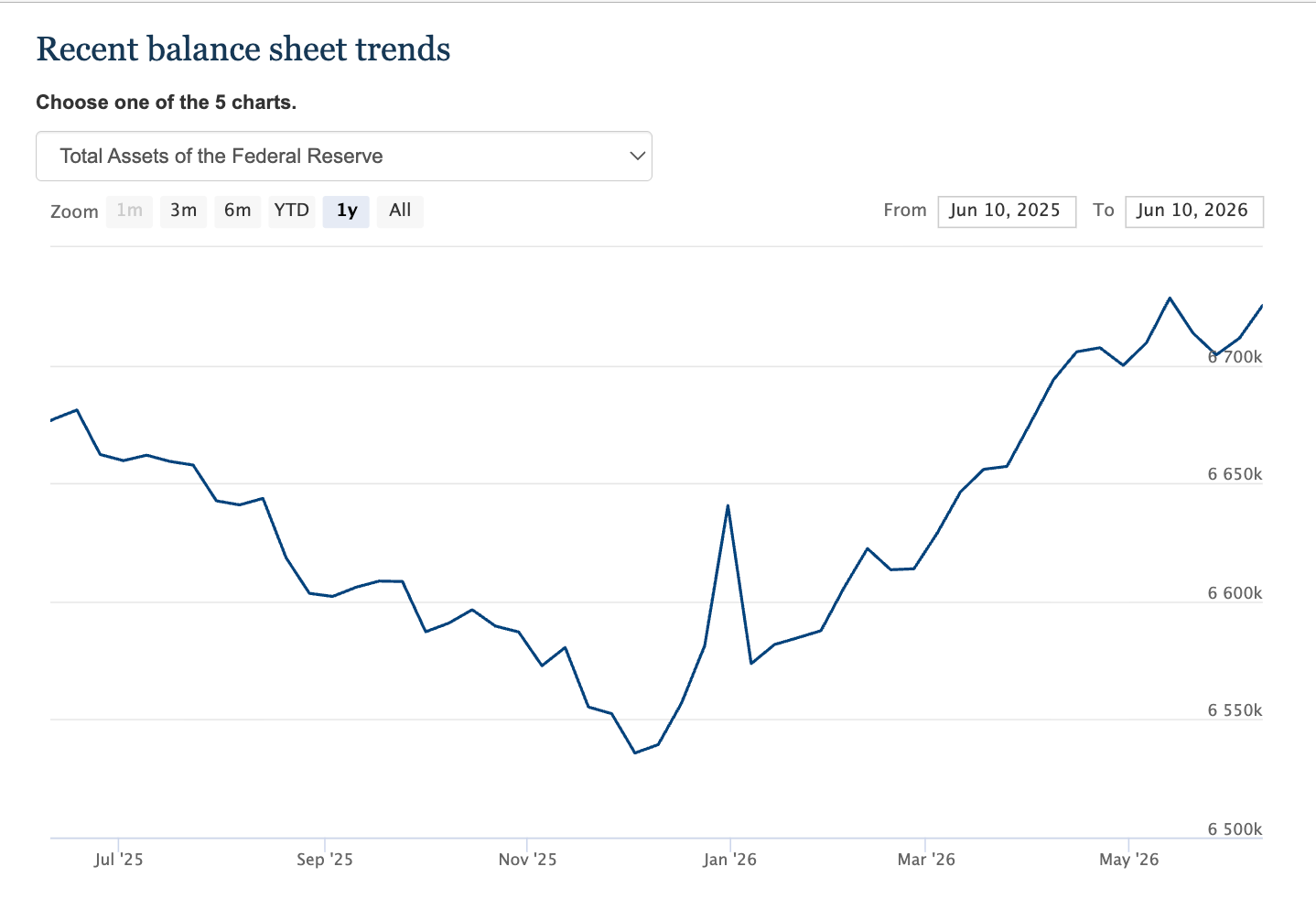

Then there’s the balance sheet. This one is a little more discreet, but became a tool of preference in the Ben Bernanke years. After the 2008 crisis. the Fed printed trillions of dollars to purchase U.S. bonds.

That helped reduce interest rates (or really stabilize them), and encouraged people to take economic risk. This was known as Quantitative Easing.

The reverse is called Quantitative Tightening, where the Fed allows bonds to fall off their balance sheet and drain money back out into the system. Warsh has spent over a decade arguing that the Fed’s balance sheet is too large, and he wants to shrink it.

But there’s a funny little thing that he’s inheriting.

Since December, the Fed has actually been ADDING to its balance sheet through a policy that looks like QE, smells like QE, quacks like QE, but doesn’t count as QE because… well they say it isn’t QE.

The Fed isn’t buying longer term bonds.

It’s buying Treasury bills and helping to keep capital in the banking sector… and instead of QE, they call it Reserve Asset Management. It’s “totally not QE,” everyone… but it aims to achieve the same outcomes as QE, which is to provide stability to the financial system.

So for roughly six months, while inflation ran above the Fed’s approved target, the balance sheet went up, not down.

There are other levers.

The Fed pays banks interest on reserves parked at the central bank, a rate called IORB, and lowering it would push banks to lend rather than hoard cash.

In today’s operating framework, IORB and the balance sheet matter far more than the reserve requirement, which has largely faded into the background since 2008.

We’ve been operating at a reserve ratio of… ZERO percent since March 2020.

The last tool is the megaphone, where a central banker looks the country in the eye and says we’ll do whatever it takes. This is more subtly known as “forward guidance.”

Words anchor expectations, and expectations drive prices… and liquidity and economic conditions appear to drive everything in the post COVID world…

Warsh’s instinct has historically been to use the microphone less, not more.

All Heading in the Wrong Direction.

Now line up those four tools against what inflation is doing…

Inflation is hot again. May headline CPI ran 4.2%, up from 3.8% the month prior.

Gasoline prices are running hot because of Iran.

And at the same time, every single tool is either idle or pointed the wrong way. Rates have been parked at 3.50% to 3.75% since December.

The balance sheet has been growing for six months, not shrinking.

IORB is still rewarding banks for sitting on cash rather than lending. And while that’s been happening, there’s been a lot more focus on containing stress in the repo market… which helped fuel stability in the final months of 2025.

How quickly we forgot about that episode… and Japan’s stimulus in November… and the RAM of the last six months… and the Treasury’s activist efforts in March.

All the while, the megaphone is leaning patient.

When inflation rises and you do all of that, the real cost of money falls.

You aren’t holding the line. You’re easing… or really “Supporting”.

The printer never turned off.

It just learned to hum more quietly.

The Real Reason for No Action.

So, why stay frozen with a full toolbox? With inflation hot and consumers looking at sticky services prices that just won’t go down…

Well…. it’s not because anyone forgot how.

Let me explain one more time…

It turns out that inflation targeting and debt management are becoming increasingly incompatible goals.

A central bank can crush inflation.

A heavily indebted government can survive higher rates.

But doing both at the same time becomes increasingly harder as the debt grows faster than the economy.

That tension, more than any individual policy mistake, is the story of life after COVID.

The numbers explain just how insane this whole situation has become…

The federal government owes more than $39 trillion. In fiscal 2025, net interest on that debt hit roughly $970 billion, which means the country now spends more servicing its debt than it spends on national defense.

But all the while, more and more bonds and Treasury bills that finds its way into the economy through the ongoing ascension of this debt… becomes a form of collateral that ends up manifesting into capital and finding itself way into driving up asset prices.

We pay more in interest than we pay to fund the entire military. Every additional point the Fed raises piles hundreds of billions more onto that bill.

The Congressional Budget Office sees interest costs climbing to $1.8 trillion within a decade. Remember, this is in the same currency that people are paid their income in… while so many live paycheck to paycheck.

All while the new debt feeds asset prices… For reasons many people don’t understand… but we keep doing our best to help them learn.

The problem now is that a true Volcker move in 2026 wouldn’t just cause a recession.

It would detonate the federal budget.

Economists have a polite term for this.

They call it fiscal dominance.

I call it the printer holding the steering wheel.

Western Asset warns clients that fiscal dominance and financial repression are the road ahead.

Bridgewater’s Ray Dalio says we’re past the point of no return on the debt, and that 1930s-style financial repression is coming. I think we’re already here.

When inflation runs faster than the interest the government pays on its debt, the real value of that debt quietly shrinks.

The gap between the two is effectively a tax you never voted for.

You pay it every time your paycheck buys a little less than it did last year. The fancy name is financial repression.

The plain name is your savings funding their bill.

What to Watch Wednesday

For tomorrow, a hold on rates is certain…

Kevin Warsh is the self-styled inflation hawk who said the Fed “helped create fiscal dominance.” Will he use his very first meeting to confirm that view?

I don’t know… but we should watch three things…

First, watch the dot plot, and whether it quietly increases rate hike expectations...

Second, watch the language, and whether “we are committed to 2%” comes with any plan to get there, or just patience, which is the polite word for not using the tools.

We’ve been told to be patient since Inflation was “transitory…”

Remember that?

Finally, watch the press conference for the only question that matters.

Whether he’ll look through 4% inflation because the alternative is unaffordable.

Tomorrow quickly tests Warsh’s stated independence.

If the new chair flinches, if he talks tough and acts loose, then the most credible hawk in a generation just told you that the trap is bigger than any one person, and that fiscal dominance won.

Inflation may be a choice.

But once debt reaches a certain size, so is the decision not to fight it.

Both parties created this problem…

Remember that… it’s not a left or right issue…

It an up or down one… and it all starts and ends with the bond market.

Stay positive,

Garrett Baldwin

Final thoughts from today…

The market narrative has shifted from geopolitics to rates and financing. That is where the next move comes from. I explained this in Money Printer Pro today.

The Fed is passively easing. Rates are flat, the balance sheet is growing, and reserve requirement at zero. Don’t forget that, because all roads point in that direction in the years ahead.

Today, the AI capex supercycle remained the dominant theme across research desks I communicated with. We have record debt funding it, with roughly $570 billion this year in new CapEx.

Power and construction, not chips, are now the real bottleneck for the buildout. But once we get there, the next layer will be… Trust.

Broadening is currently the market’s hope, but not showing up in the tape. Leadership keeps narrowing back to Semis and Mega-cap stocks right now.

Japan is the quiet giant. The BoJ went to 1% today, and I remind you to watch the Forex market. A big jump in repatriated capital could drain global liquidity and compress valuations very quickly. The crisis starts in the currency markets.

Two risks to watch… We have a very thin book and a 4% gamma cliff. Now, we will start to discuss the fiscal-dominance trap at scale.

Right now, we want to stay long the earnings engine, but it’s a good time to hedge. Keep your downside hedges on, and don’t chase the peace.

To join us at Money Printer Pro… click this link below. You can get a deeper dive into the stories above as we continue to focus on the way these markets have changed.

Song For Trading the Federal Reserve Tomorrow…

Thank you Garrett for the preview of Kevin's call and the peep at Peach Pit. I'm now a fan.