Thank you John Watkins, Harish, Mike Curatolo, Ron Lazar, Stephen Berman, and many others for tuning into my live video! Join me for my next live video in the app.

Good morning…

I’ll do a live breakdown of the CPI this morning… This is quite an interesting market. Nearly every trading desk that I’ll read or chat with doesn’t trust the bounce, and the primary reason lives within this CPI.

The futures market has only priced in about a 25-basis point hike from the Fed by December. So, we don’t have any meeting yet by the Fed, we have increasingly hawkish talk, and it’s a market that’s holding a lot of room to reprice.

Markets have expected two to three hikes out of the European Central Bank, and two from the Bank of Engladn. Rate hike expectations have the capacity to whipsaws stocks. The Fed could do nothing next Wednesday, but the damage still comes from the curve repricing.

We have an expectation for a CPI core at 2.9%, though I’ve seen some weaker forecasts. We could have a similar situation to last week’s jobs report where there’s a scary headline number (4% is the line in the sand for the primary CPI), but we have a calmer core figure.

A hot core reinforces higher-for-longer and likely reloads the selling.

A soft core is the off-ramp.

Right now, our attention is on momentum, which is bouncing around. Friday’s crash was mechanical.

Leveraged-ETF rebalancing forced over $50 billion of selling, and the semis went in the most stretched since the dot-com era.

But then, the market bounced almost perfectly off 7,400 on the S&P and 28,800 on the Nasdaq. Remember, I say all the time that markets don’t go straight down. They hit moving averages and they bounce. That happened yesterday on the SPY with the 50-day moving average

The thing that still has my attention is that most trend-following funds are still VERY long and only about 5% from the triggers that force more selling.

One last thing… before we get to the analysis. People are asking me about silver.

I’ll discuss what’s going on during our conversation today…

Traders Focus

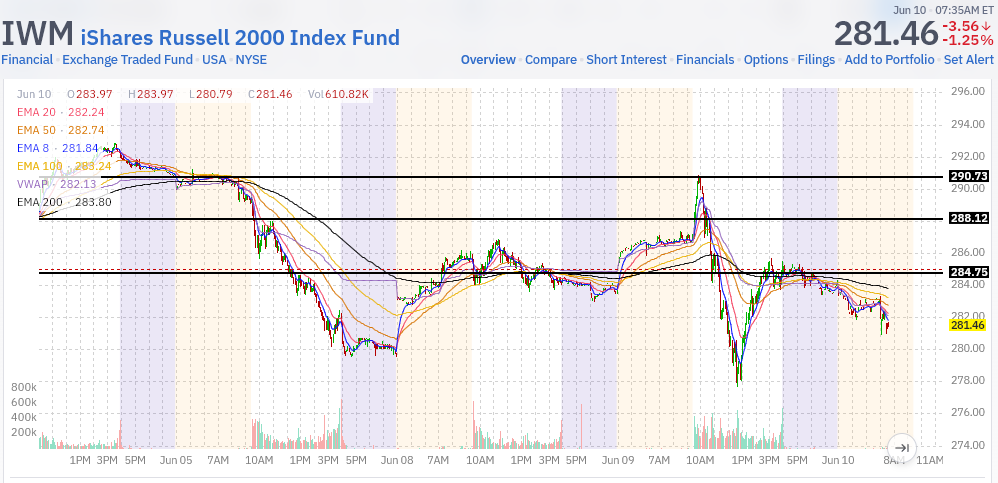

Friday changed the character of this market. After a hit like that, the first thing we do is mark every spot where it broke down and every spot where a bounce failed. Those points become the roadmap, because the trend does not shift back in our favor until price climbs back above the levels it broke down from.

Funds get caught off guard on a move like Friday, and you usually see the first bounce come as a get-me-out-of-this-market move. We marked these levels on Monday.

Tuesday, the Russell rallied back to where it failed and rolled over again. Until we are back above 291, these bounces are just noise inside a larger downtrend.

We’re in a pattern of lower highs and lower lows across all three indices, and that has to break before we put real risk back into this market.

Chasing a market like this, with weakening momentum and spotty liquidity underneath it, is how you end up a bag holder.

So we’re watching for what changes this. It could be a headline out of Iran, maybe Japan deciding not to hike next week. Right now, we do not have it, and everything on the board still points lower.

Once again, the FNGD called it.

It warned us on the 4th when it popped above its 8-day, and it is now pushing toward its 50-day. The S&P is down 2.7% in that time. The FNGD did its job again.

You can see the result in the MAGS, the Roundhill Magnificent Seven ETF, now pulling back beneath its 100-day. The next support for the MAG-7 is the 200-day. The damage is getting deep in the biggest names in the market.

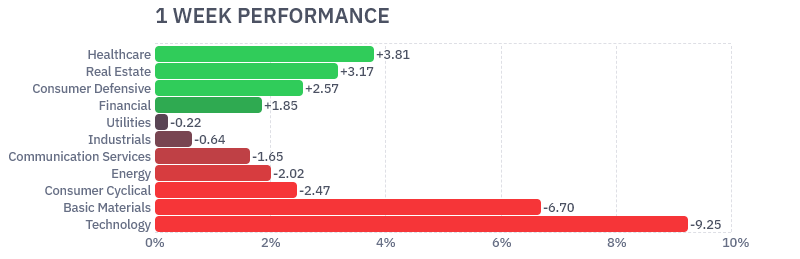

The saving grace is that a good chunk of this money is rotating rather than running for the door. Health care, real estate, consumer staples, and financials are all working this week, with everything else struggling. That keeps our reading yellow rather than red, but it is a risk-off kind of yellow.

On the screamer list this morning, nothing looks the same as it did a week ago. Quest Diagnostics (DGX) is a new one to watch, sitting at the top of our triple screener and breaking out, up about 8% over the past week and 10% over the month.

On the breakdown side, CF Industries (CF), APA, and Palantir (PLTR) are rolling over. Albemarle (ALB) is on day six at the top of our crashers, now back to its 200-day. At some point this becomes a buy again after the run it had, so it is worth deciding what price you want. Around $135 is where you could start to nibble.

Lithium Americas (LAC) is another, cheaper shot on the lithium story, also trading under its 200-day. Figure out where you are comfortable starting. Under $4 is a good price on LAC.

On the launchpad, Pilgrim’s Pride (PPC) is still set up and looks ready to go. It is hitting resistance at $30. If it can clear that, the 50-day is next with a little resistance, and then it could find its way back to the 200-day.

The VIX is riding a widening pattern right now. You can draw a straight line down the middle around 18, and it is sitting at the top of that widening range.

If the trend holds and CPI gives any relief, it pulls back toward that center line, and from there it decides whether it wants the bottom of the range or another run at the top. Keep an eye on it, because if it holds these lines today, we have a new setup to trade on the VIX until it breaks. You could use the UVXY/SVXY as the trading instruments there.

The tempo, once again, is to take it easy into the open. Let the dust settle and trade the CPI reaction around VWAP. If it comes in hot, the defensives keep working and the pressure stays on big-cap tech, the metals, and the stuff that does not throw off yield, because rising hike odds make people want assets that pay them to wait.

We are not going to force anything here. We sit on our hands until this market gives us a reason to act.

Market outlook

Treasuries little changed as markets brace for May CPI; core inflation expected to show inflation jumping to 4.2% from 3.8%

Chip-trade reversal deepens; SMH puts forcing market-makers to short, echoing the feedback loop that drove the rally higher, now in reverse

SpaceX (SPCX) signs $920M/month Google deal to rent GPUs days ahead of its June 12 IPO

Super Micro (SMCI) falls 9% after hours on plans to raise $7B to fund parts costs; company touts $39B in recent AI server orders

GM pivots EV battery capacity toward grid-scale storage, partnering with Peak Energy on sodium-ion batteries to serve AI data centers and utilities

China moves to curb record outflows with new offshore-investing restrictions rerouting activity toward Hong Kong

Sycamore Partners in talks to sell Boots for $10B a year after Walgreens buyout per FT; deal would scrap planned London IPO

Robinhood (HOOD) cleared to act as an IPO underwriter, opening a new revenue stream beyond its retail role

Momentum - Fragile Yellow

Tuesday was violent and two-sided. The S&P cracked early, falling all the way to its 50-day line before bouncing off it and climbing nearly 2% off the lows into the close. The momentum reading went hard negative intraday, then clawed back to green by the bell. A deep drop and a sharp bounce in the same session don’t happen often, and they’re the mark of a market with no firm footing.

The bounce was broad, which was the good part. By the close nine of eleven sectors were green, led by real estate, healthcare, and industrials, and the S&P’s equal-weight reading, the average stock, finished sharply positive. The Russell came with it, its trend back in the green.

What the bounce didn’t reach is the problem. The mega-caps never recovered. Microsoft, Amazon, and Tesla closed lower, Tesla down 3%, and the big-tech ETF broke under its 100-day before a late crawl back. The cap-weight readings stayed negative, money still bleeding out of the names that led the whole rally.

The fragile part is already showing. The bounce hasn’t carried into this morning. The daily readings rolled back over overnight, the broad equal-weight number that surged Tuesday is negative again, and the S&P’s cap-weight trend has tipped negative. The Nasdaq’s trend has slipped just under the line with it. The green didn’t last the night.

The level to watch is still 7,400 on the S&P, and CPI lands this morning into a market that’s already rolling back over. That raises the stakes on the print.

A hot number on top of this morning’s weakness leans hard on the mega-caps that never stopped bleeding. A soft one is about the only thing that pulls the bounce back. Tuesday held the line. This morning it’s handing some of it back, and CPI decides whether that’s a wobble or the start of the next leg down.

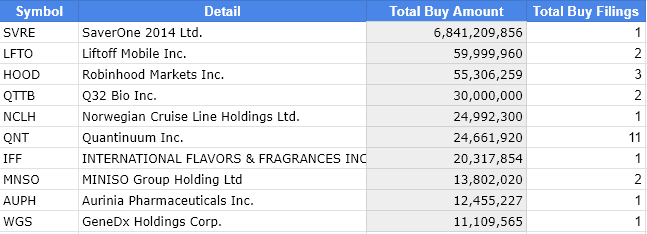

Insider Buying: Better Day, Malka Buys More HOOD

The ratio of Buys to Sells: 1:5 (87M to $414M)

Top Buy: $30M of Liftoff Mobile (LFTO) by 10% Owner General Atlantic Genpar

Top Sell: $85M of Circle Internet Group (CRCL) by Director Sean Neville

Top Insider Buys of Last 10 Days - Form 4 Documents

Market Liquidity

Since March, the two-year Treasury has traded above the Fed’s own policy rate, and the gap keeps widening as the data runs hot. When the market charges more for money than the Fed does, it’s telling you the Fed is behind.

What’s being repriced isn’t just a hike or two. It’s the idea of what restrictive even means. The Fed has assumed its rate is holding the economy back, which is why it kept leaning toward cuts. The market sees it the other way. With the AI buildout pumping money into an already-hot economy, the rate that actually restrains anything has drifted higher than the Fed thinks. By that math, today’s policy isn’t tight at all. It’s about neutral, and rates would have to rise just to start biting.

That’s why oil falling hasn’t bought any relief. The market has stopped trading the data and started repricing the framework itself, and that pulls the whole curve, not just the front end. CPI lands this morning, and the core reading will feed it either way, but even a soft print doesn’t change the bigger message. A 4% handle across the curve is starting to look less like a spike and more like the baseline.

Warsh built his case on policy being too tight and cuts coming. He walks into his first meeting next week facing a market that’s already decided he’s late. The gap between where the Fed thinks neutral is and where the market thinks it is, that’s the real story now, and it prices everything downstream.

Stay positive.

Garrett Baldwin