The Big Short... 2.0

JPMorgan is looking for new and fun ways to profit from a collision course in AI.

Dear Fellow Traveler:

Well, I wanted to start today by stressing the futility of morning shows on YouTube.

There’s a whole permanence to it all, and they don’t necessarily prioritize morning content that becomes stale within a few hours… So, I pivot like I’m used to doing…

We’ll keep the channel active here… and run videos a few times a day. They’re free, so you can just go there…

Failing fast and turning to places where I know that people are paying attention. In the video above (which is quite beautiful and doesn’t require my face)… I outlined something that really caught my attention in recent weeks - and will likely persist for the months ahead.

JPMorgan - that bastion of innovation and “we didn’t do anything wrong in 2007” is doing the thing that they said they didn’t do… Allow rampant speculation around a massive asset class that is carrying the U.S. economy right now.

In 2008, housing was the story…

Today, AI is the linchpin of new economic growth. So, JPMorgan decided in March to do what is best for Wall Street. It created assets to bet on an outcome in which companies scaling up these AI data centers will… fail.

The Casino Annex

Here’s what’s wild about JPMorgan starting this process and all of our attention to what’s going on with Meta’s debt.

A few days ago, Warren Buffett was in Omaha and telling 40,000 people that he’s never seen Americans in “a more gambling mood.”

Berkshire is sitting on $394 billion in cash because it can’t reasonably find anything worth buying. Buffett called the market “a church with a casino attached.”

It was The Big Short that took a moment to explain how CDS and CDOs all work. There was a scene involving Blackjack in which the side bets on the original bets were placed.

JPM is doing the same thing.

Their product around AI debt is effectively a side bet on whether the biggest companies in the world can pay back the money they’re borrowing to build something that doesn’t yet generate returns.

And that to me is just a perfect representation of where we are right now as people.

For anyone new…

The AI debt product is a basket of credit default swaps on the debt of Alphabet, Amazon, Meta, Microsoft, and Oracle.

A credit default swap is insurance on someone else’s debt…

I stress someone else’s debt…

And then I stress the other part that isn’t in the description…

You don’t actually have to own the debt, be involved with the company, or even understand what the company does.

You pay a premium to bet against it... (although some genius at a bank somewhere will tell me that these assets are used as hedging mechanisms by advanced mathematical risk portfolios and that I need to read the prospectus).

Which I remind them… Yeah… We both know what it does, bud…

But let’s really lay this out and judge it not by intentions or strategy…

But by the outcomes…

And the outcome is that if the debt deteriorates, the CDS owner makes money....

It is like buying life insurance on a stranger and then checking their MyFitnessPal every morning to see if they have a heartbeat.

And then, for some CDS buyers, being mad if they do...

How We Got Here So Fast

We said we weren’t going to do this again, remember?

We got back in record time.

The housing bubble took about 15 years to build the full derivatives ecosystem.

Mortgage-backed securities started in the 1970s.

CDOs emerged in the late ’80s.

Credit default swaps on mortgage bonds didn’t become a speculative playground until the early 2000s. And it took regulatory hijacking to make it possible.

It took Wall Street three decades to get from “here’s a mortgage” to “here’s a synthetic bet on a tranche of mortgages we don’t own inside a structure that references other structures.”

AI did this in a little less than three years.

We went from “ChatGPT is neat” to “JPMorgan is packaging credit default swaps on the five companies building AI infrastructure” in the time it takes most people to finish remodeling a kitchen or to author a poorly written novel...

The buildout isn’t even done yet, and the returns on AI haven’t been proven.

But the derivatives desk has already built the exit… and the tools for collapse...

That’s not a red flag in the traditional sense…

It’s more like the market is admitting, through its own plumbing, that it doesn’t fully believe the story it’s telling with equity prices.

If we look at the numbers underneath this thing, it tells us how incredible things are getting here… and why we need to pay attention.

Morgan Stanley’s capex forecast for the Big Five hyperscalers is $800 billion for 2026 and $1.1 TRILLION for 2027.

Recall… most of the financial system doesn’t actually finance growth.

As Howell said yesterday, we’re built on the back of a refinancing system…

And that refinancing system requires competition for the dollars needed to refinance.

The government is crowding out parts of the private sector regularly…

And now… we have these companies going to the debt market, even as we already know about problems in the government, commercial real estate, and private credit.

The other issue is what this buildout does represent…

These companies used to be the cash cows of American markets...

Now, Amazon’s free cash flow has collapsed, and Meta’s is projected to go negative in 2026.

So, the whole buildout is being funded by the bond market… which is absorbing tech debt at 18% of total investment grade (IG) supply, the highest share on record…

And it’s all happening at a pace that made April’s issuance come in at nearly double the estimate.

The banks distributing this paper can’t keep up.

As I explained above, JPMorgan and MUFG spent six months trying to place $38 billion in Oracle data center debt.

For context, who hasn’t had relationships that lasted less time and were less stressful for everyone involved?

The co-head of credit risk sharing at Man Group said the sizes are “out of scale to anything we have ever thought about,” which is the kind of quote you usually hear right before the part of the documentary where the screen goes black and a subtitle tells you what date everyone went to rehab...

Are We Really Okay With Oracle Debt?

Oracle is Larry Ellison’s database company.

It’s the company that your IT department has been trying to migrate away from since 2014…

Well, it’s now the No. 1 name in the entire investment-grade bond index by duration-weighted exposure.

I don’t even know how that’s mathematically possible or socially responsible...

Goldman Sachs said this week that 11 issuers now account for a quarter of all duration-adjusted investment-grade supply… The investment-grade bond market was supposed to be the boring one.

Now it has what feels like the Nasdaq's concentration profile, except you don’t get any upside if AI works. You just get your money back.

If things go well, you earn a coupon. If things go poorly, you’re Oracle’s largest creditor, and you’re explaining to your clients why their “conservative fixed income allocation” is 20% data centers.

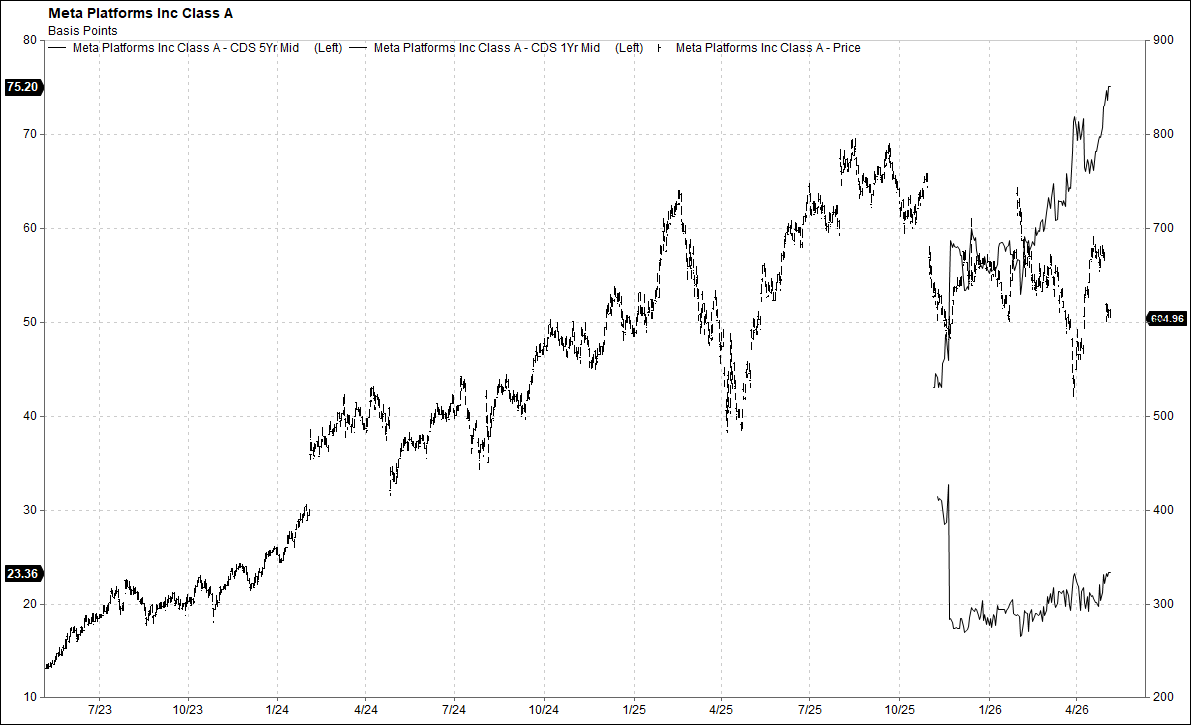

Meanwhile, Meta’s five-year CDS are just going higher and higher…

All while equities are at all-time highs.

Something isn’t adding up… is it?

Stocks say everything is great. The bond market is quietly buying insurance.

And I’ve been doing this long enough to know which one I trust when they disagree.

I’m Perfectly Calm, Dude

Calm down, Garrett… I hear some of you saying…

I’m calm…

Yes, I know… these aren’t subprime CDOs.

These are enormous, profitable companies with real revenue, and comparing them directly to 2008 is lazy.

I know that.

The underlying credit quality is different, and that matters.

But the behavioral pattern is the part I can’t get past.

Every speculative cycle follows the same choreography…

We start with a narrative, then there is borrowing, then a lot more borrowing.

Then we get the derivatives…

Then we take derivatives of derivatives.

Housing took 30 years to run that sequence.

And crypto ran it in about fivish...

AI is running it in a little less than three.

We keep speedrunning the financialization phase because Wall Street has gotten better at building the instruments… We have more ETFs than stocks…

We have more leveraged ways to bet on Meta stock than ever…

Why not increase the number of ways to bet against the debt…

Sounds fun…

But few people ever ask if building all this faster is the same as building them smarter.

And remember… this is how you end up with people in a few years saying… “This is a Black Swan event… no one saw any of these problems coming…”

Well… in a world of credit cycles and liquidity movement, something is eventually coming. And Morgan Stanley says if credit markets lock these companies out, the AI supercycle ends.

And if that’s the case, what exactly is any of this stuff really worth?

And do we end up firing up the money printer again to bail out… AI?

Which in the end is really just a bailout of the debt… that we needed in the first place to build… all while replacing the humans who would be paying off the debt…

My head hurts with all this math…

The fact that JPMorgan built a product to trade that exact scenario tells you that somebody inside the machine thinks it’s worth pricing.

The AI boom hasn’t even proven it works yet.

But the craps table is open for business…

Stay positive,

Garrett Baldwin

It makes my head hurt also. If something can’t go on forever, it won’t. Keep one hand hovering on the sell key and the other on the door out.

Didn’t Mike Burry have to cajole banks into selling him MBS insurance? And then banks ramped up selling cheap insurance? Which almost lead to a Nobel Prize on the hypothesis that cheap insurance meant housing was solid? And of course banks got killed when they had to pay up on cheap insurance?