Is America's "End Game" in This Chart?

More Saturday work from a pool...

Dear Fellow Traveler:

I'm a pretty optimistic guy.

I do my best to stay out of politics.

I use my knowledge of finance and markets to point a camera at the world…

All I’ve wanted to do for two years is launch a BIGGER newsletter that reaches people far and wide, showing them what I see.

We’ve remained intimate… at Me and the Money Printer… but we’re gaining steam -

Since I've moved back to Maryland, we’ve avoided the Nikkei Crash, and we were on top of the market downturn on February 21 when our signals went red.

We regained momentum on April 23, as I stated, and the markets continue to run.

But remember... my analysis is the newsletter publishers say “can’t be sold…”

Well… today… everyone should pay attention….

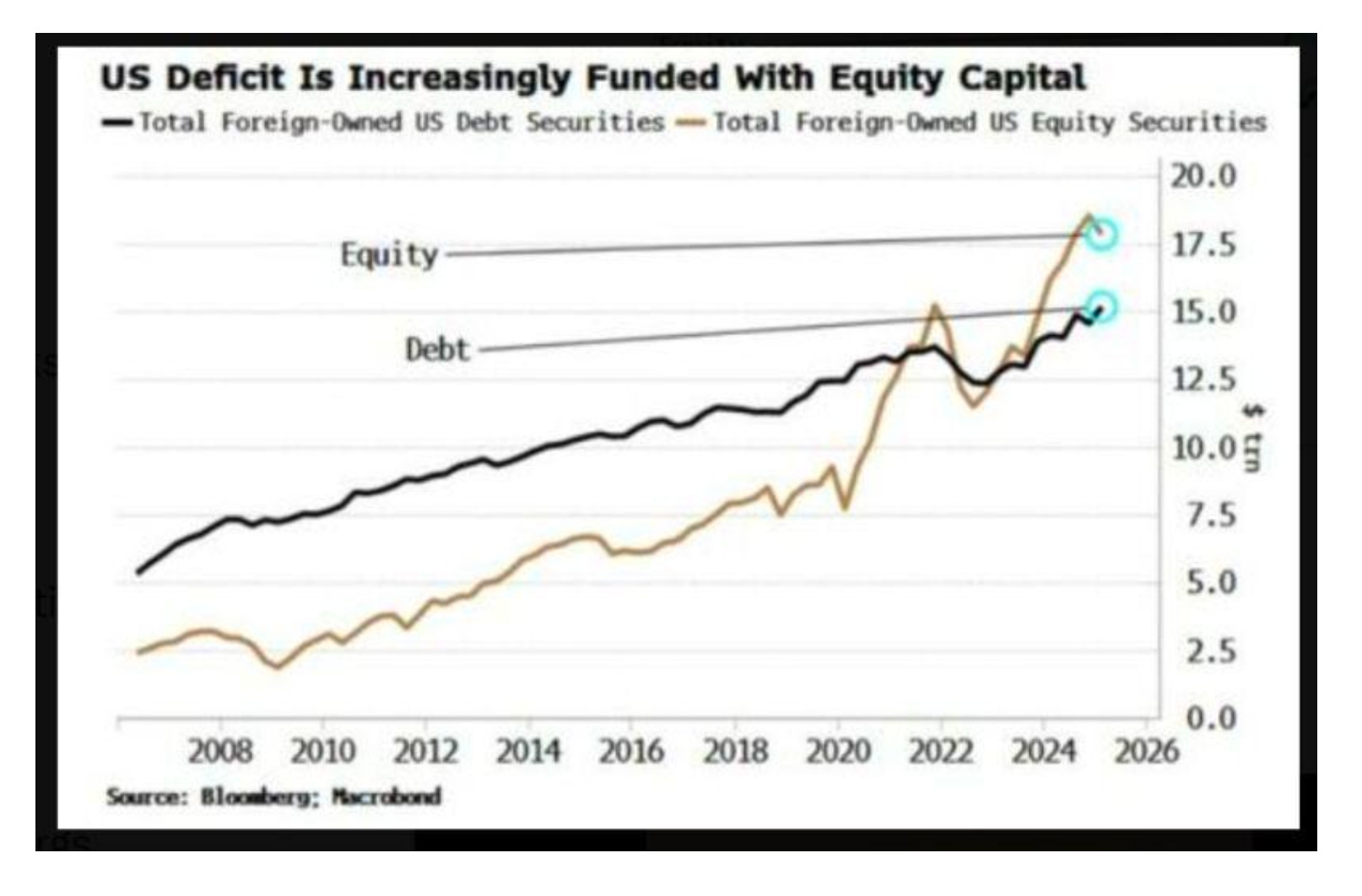

Foreign Investors Now Want Assets… Not Debt

I'd like you to look at this chart from Bloomberg.

The data shows something concerning without any embellishment.

As of 2024, foreign investors hold roughly $17.5 trillion in U.S. equities and $15 trillion in debt securities.

This divergence has widened since the pandemic, according to Bloomberg and the U.S. Treasury.

Consider this shift since the pre-COVID years…

Since 2020, foreign equity holdings have taken an elevator up while debt holdings have expanded more slowly.

This isn't routine portfolio rebalancing by global investors…

What foreign investors are saying is this…

We don’t want your debt.

We want to own… your assets.

The Unintended Consequences

The timing of this chart isn't coincidental.

The Treasury Department accelerated its shift toward shorter-duration bills, beginning around 2020.

This practice altered the value proposition for foreign investors, coinciding with a surge in deficits. (Remember, this began in 2017.)

The Treasury Borrowing Advisory Committee says that during the COVID-19 pandemic, the government increased its reliance on T-bill issuance (U.S. debt that matures within one year).

They aimed to reduce the bill share back to 15-20%.

But it is now at around 21-22%, well above its target and distorting investor behavior.

Bank of America believes it will reach 25% in the years ahead, particularly with the introduction of the One Big Beautiful Bill.

This is significant… because of the feedback loop that it creates.

The first thing that matters is the yield compression on our debt.

Long-term Treasuries would offer foreign investors a solid yield compared to their domestic bonds. Bills give investors like them minimal advantage, especially when we factor in currency hedging costs.

The constant rollover required for short-term investments creates transaction costs and reinvestment uncertainty for investors like sovereign wealth funds.

They don’t want this… So, long-duration investors like pension funds and SWFs are now on the sidelines since they don’t want a lot of rollovers or duration-matched liabilities.

What you might not know is that SWFs and pension funds NEED longer-term bonds to help them align with their long-term liabilities and payouts.

When the Treasury shifted to bills, it stopped offering what these investors wanted.

So… foreign capital had to go somewhere…

It went into this global equity rally.

When Cheap Money Meets The Herd

Treasury's shift toward short-term debt has changed the way we fund markets.

Short-term debt helps build leverage, particularly in equity-linked strategies.

As the Treasury floods the market with short-term bills, it affects short-term funding.

While the Federal Reserve controls policy rates through its interest rate policies… the Treasury’s huge T-bill supply can create volatility in funding markets. In addition, it will impact the cost and availability of financing for leveraged positions.

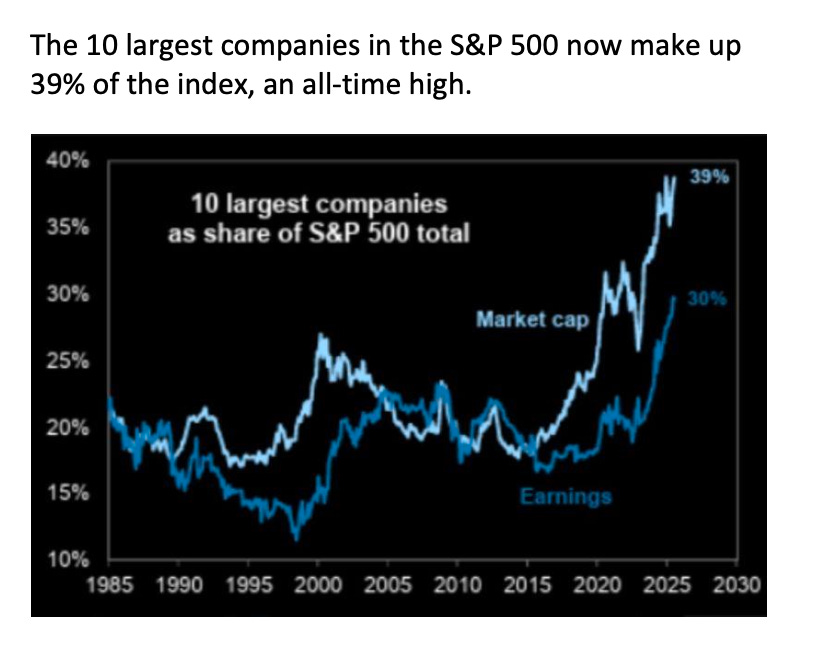

Foreign capital is more and more exposed to the same tech-heavy trades.

But this isn’t by their design.

This is because index structures and passive flows have become increasingly concentrated in mega-cap technology names. It goes like this…

Think of this like a cake.

Layer 1 - Institutional Leverage

Hedge funds and institutional investors use repo markets and prime brokerage financing to leverage positions in the same tech names that attract foreign investment through index products.

Changes in the funding structure will impact the cost of all this leverage.

Layer 2 - Corporate Leverage

The same tech companies that receive foreign investment through index flows also use corporate debt to fund aggressive share buyback programs. Yeah, they’re buying their stock back with cheap capital and cash flow.

This creates leverage within the companies that are targets of leveraged investment strategies. Isn’t finance awesome?

Layer 3 - Synthetic Leverage

Now, let’s bring in the derivatives… and options…

This new later provides MORE leverage onto the same underlying positions through options flows, equity swaps, and structured products.

This is all concentrated in the most liquid tech names. And it’s why on Triple Witching Day every quarter, you’re seeing trillions and trillions of dollars of contract expiration happening at the same time. It’s manic.

Layer 4 - Index Concentration

Oh… don’t forget about all the money flowing into passive investments.

That includes the money from foreign investors that is pumping money into market-cap-weighted indices. These ETFs and other funds all concentrate on the same stocks because many of them aim to replicate the S&P 500 and its benchmark.

This creates a vicious feedback loop that helps push prices higher and higher, forcing ETF rebalancing, which in turn creates more buying and higher prices.

And that’s where all the crowding accelerates.

Multiple forms of leverage and concentration build upon each other.

They’re all centered on the same stocks and same contracts.

Everyone thinks they're in different trades, but they're all exposed to the same names, potentially vulnerable to similar shocks. This is why I watch the FNGD.

For when the music stops...

When the Music Stops

The data reveals how this new financing model has evolved.

Foreign debt holdings continue to grow.

But they've grown more slowly and reluctantly.

Meanwhile, the dramatic rise in foreign equity exposure since 2020 highlights America's growing dependence on volatile capital flows into stock markets…

It’s no longer about government bond purchases. No one wants that paper…

This setup creates several plausible scenarios for the future…

Funding stress: If short-term financing markets seize up, leveraged positions across multiple layers might need to be unwound simultaneously. This was what happened in 2008 and 2020. But also 2024 with the Nikkei… oh and well, every other crash…

Correlation collapse: In a crisis, all these "different" strategies could become perfectly correlated as everyone tries to exit similar crowded positions. This is where stocks and bonds all drop in price at the same time… This happened in 2020, 2022, and 2025. Yes…

Liquidity dynamics: During forced selling, the most liquid names become the easiest to sell, making them the first to fall, and fastest to magnify volatility, as they're the only names large enough to absorb the selling pressure from deleveraging.

These are the lessons of 2020 and 2024. Again… watch the FNGD as a clue.

Foreign flow risk: Unlike government bonds, equity positions can be liquidated quickly. Foreign investors spooked by market volatility or geopolitical tensions can trigger rapid capital outflows from equity markets. With the U.S. now representing about 67% of the global equity market… that bubble is big…

And proof that AMERICA is the bubble. Not AI.

Now… For Policy Implications

It’d be great if we could have a conversation about this, but I feel that too much attention can create social media panic. All we need is a bunch of Wikipedia experts now suddenly becoming an expert on the financial plumbing of the system…

Everyone… everywhere… now… soon… an expert on Reverse Repo…

The issue, though, is that this concentration in bill governance has created consequences… It’s:

Reduced the stability of deficit financing

Increased dependence on volatile equity markets for foreign capital attraction

Contributed to an environment that enables massive amounts of leverage

Increased concentration risk in the financial system… as evidenced by this chart…

A gradual return to longer-duration issuance would increase the Treasury's short-term borrowing costs.

But it could provide more stable financing and reduce some systemic risks.

But it could also crash the equity market or lead to a pronounced unwind…

Is This The Endgame?

Considering how this market works, it now feels like a late-cycle setup to an endgame. But the potential scenarios are not great…

Scenario 1: You Get a Controlled Unwinding

In this situation, the U.S. Treasury acknowledges the systemic risks and gradually shifts its focus back to longer-duration issuance. Bond yields go much higher…

Foreign appetite for U.S. debt slowly returns as bills are converted back into bonds.

Leverage gradually deleverages as funding costs normalize and the crowded trades thin out.

Equity markets correct but don't crash.

This requires effective policy coordination and a strong political will.

Good luck with that… We saw what happened when the 10-year bond hit 5% in late 2023. Imagine what our economy looks like with a 10-year yield at 6% or higher…

It’ll be wild in the housing market…

Scenario 2: Crisis-Triggered Unwind

An external shock, such as geopolitical tensions, recession, or financial stress, triggers forced selling in leveraged positions.

The unwind cascades across multiple layers: institutional deleveraging, corporate buyback suspensions, derivatives unwinding, and index selling.

Foreign capital flees both equity AND debt markets just when America needs it most.

Liquidity deteriorates in the most "liquid" names, creating severe volatility where mega-cap tech stocks become the transmission mechanism for broader market stress.

In a worst-case scenario, the Fed might need to intervene again - reminiscent of past liquidity crises.

Given that they’ve done so over and over, most investors would expect the Fed to step in. But what happens if all these investors double down and the Fed doesn’t?

That’s some 1929 style stuff…

Scenario 3: This is The New Abnormal

Drink up, everyone.

Because - for now - this is what I think we’re facing.

This is now America's permanent financing model. It’s volatile, leveraged, and concentrated. And you’d better be playing by its rules.

The U.S. economy adapts to its dependence on equity market funding, characterized by periodic (annual?) boom-bust cycles as leverage builds and unwinds.

Financial instability becomes the price of financing flexibility, with more frequent but "manageable" crises.

And by manageable, I mean predictable…

So, follow us… because I’ve been doing this for a few years - and Me and The Money Printer remains honest about how this financial system really works…

It’s you and me… on the road… managing this madness one mile at a time…

Stay positive,

Garrett Baldwin